Sorry, but your login has failed. Please recheck your login information and resubmit. If your subscription has expired, renew here.

December 2024

I am just weeks away from completing my second year as editor-in-chief of Supply Chain Management Review. It has been a fast two years—I can say that with certainty. Perhaps that’s because of all of the changes the industry—and the world—have undergone during this time. If anyone thinks that business moves slowly, they are mistaken. Browse this issue archive.Need Help? Contact customer service 1-508-503-1313 More options

The results of our annual Warehouse Operations & Trends Survey are back, including a healthy uptick in the average capital expenditure budget for enhancing DC networks, equipment and systems.

Beyond the positive trend on budgets, there’s a more fundamental change one can see in the findings: less reliance on paper-based methods, and high adoption of software and automated means of generating metrics.

Following are just a few highlights.

• Projected capex budgets rose from an average of $1.15 million last year, to $1.8 million this year.

• This year, 93% of respondents told us that they use some type of warehouse management system (WMS) software. That’s well over the usual mid-eighties percentile we get on that question.

• Reliance on paper-based picking plummeted, down to 44% of respondents, after trending near the mid-fifties percentile range the previous three years.

• When asked about top challenges, 45% cited “outdated storage, picking, or material handling equipment” as a major issue, a 10% increase versus last year’s survey.

All that sounds bullish, but the survey also shows respondents continue to struggle with issues like inventory management, including a drop in turns this year even as SKU counts are trending down.

Related presentation

SC

MR

Sorry, but your login has failed. Please recheck your login information and resubmit. If your subscription has expired, renew here.

December 2024

I am just weeks away from completing my second year as editor-in-chief of Supply Chain Management Review. It has been a fast two years—I can say that with certainty. Perhaps that’s because of all of the changes… Browse this issue archive. Access your online digital edition. Download a PDF file of the December 2024 issue.The results of our annual Warehouse Operations & Trends Survey are back, including a healthy uptick in the average capital expenditure budget for enhancing DC networks, equipment and systems. Beyond the positive trend on budgets, there’s a more fundamental change one can see in the findings: less reliance on paper-based methods, and high adoption of software and automated means of generating metrics.

Following are just a few highlights.

- Projected capex budgets rose from an average of $1.15 million last year, to $1.8 million this year.

- This year, 93% of respondents told us that they use some type of warehouse management system (WMS) software. That’s well over the usual mid-eighties percentile we get on that question.

- Reliance on paper-based picking plummeted, down to 44% of respondents, after trending near the mid-fifties percentile range the previous three years.

- When asked about top challenges, 45% cited “outdated storage, picking, or material handling equipment” as a major issue, a 10% increase versus last year’s survey.

All that sounds bullish, but the survey also shows respondents continue to struggle with issues like inventory management, including a drop in turns this year even as SKU counts are trending down. For certain, the survey shows respondents want to do better with inventory management, while also tweaking DC networks. Finding labor continues to be a top challenge—not only in terms of finding and retaining front-line associates, but also for supervisors.

The survey, conducted annually by Peerless Research Group (PRG) on behalf of Logistics Management and sister publication Modern Materials Handling, asks about operational factors at DCs, such as size of the DC network; number of employees; average annual inventory turns; use of temporary labor; strategies for coping with peak demand; and other challenges such as finding and retaining labor.

This year, the survey drew 108 qualified responses from professionals in logistics and warehouse operations across multiple verticals. The survey was in the field during August of 2024. The average company size among respondents did not change significantly this year, though industry makeup saw some slight changes.

Overall, the survey reflects that technology adoption is moving forward, and that, as a result, there’s a more data-driven approach to management, observes Norm Saenz, Jr., managing director and a partner with St. Onge, a supply chain consulting firm, which continues to help us by reviewing the findings and helping to spot trends.

“We see companies moving more and more toward using systems and software, and having a foundation for analyzing data,” says Saenz. “There are clear signs of that trend in this survey, like the drop in reliance on paper-based systems. Sometimes the mix of respondents may bring in a few more companies with advanced systems, but overall, the industry has been adopting more technology, including software and automation.”

Operational profile

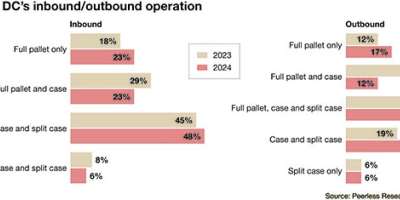

On the inbound side for 2024, 23% handle full pallet only, compared to 18% last year, while 23% say they deal with full pallet and case, down from 29% last year. This year, 48% deal with a mix of full pallet, case and split case inbound, while 6% deal with case and split case, making 53% who handle either case and/or split case to some degree on the inbound.

On the outbound side, 17% ship full pallet only, up from 12% in 2023, while 11% ship full pallet and full case outbound, down from 30% last year. Meanwhile, 35% say they ship a mix of full pallets, cases, and split case, up from 33% last year. Case and split case outbound rose to 31% this year, up from 19%, while 6% do split case only outbound, same as in 2023.

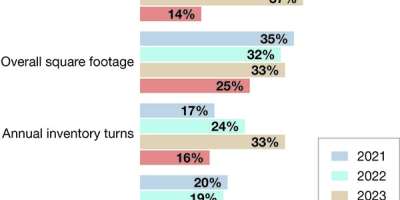

In terms of total square footage (sq. ft.) in the DC network, the average came to 408,020 sq. ft., compared to 479,565 sq. ft. average last year. The average annual revenue size for respondents’ companies this year, at $774 million, is just under last year’s average of $778 million.

When we asked about the most common square footage in the network, the overall average was 198,558 sq. ft., up from 169,140 sq. ft. last year.

When there are three or fewer DCs in the network, the average square footage was 220,000, down from a 227,100 average last year. When the network has four or more buildings, the average this year was 811,200, up from a 423,315 sq. ft. average last year.

In terms of the number of buildings in the DC network, 42% this year tell us that they have just one, up from 32% the year before. For 2024, 21% had two buildings, compared to 17% last year; 14% have three buildings (up from 8% last year); and 23% this year say they had three or more buildings, down from 43% last year.

We ask about the clear height trends by giving respondents five ranges to select from as most common: under 20 feet; 20 to 29 feet; 30 to 39 feet; 40 to 49 feet; and 50 feet or higher. This year, the average came in at 29.6 feet, down from 31.3 feet last year. This year, 42% said average clear height was in the 20- to 29-foot range, up from 33% last year.

The average number of employees in the main DC once again edged up, from an average of 132 employees last year, to 146 this year. Again, we present ranges for this question. This year, while 25% reported fewer than 10 employees, a combined 15% had an employee count of 200 or more.

Overall, observes Saenz, the findings on operational profiles didn’t change drastically, though average square footage did edge up. One possibility is that some respondents are adjusting network strategies, and might end up with slightly fewer buildings, but perhaps some bigger DCs with more automation. “Generally, when you have a larger building, that can make it easier to justify certain automation projects, so that might be a factor at work here,” says Saenz.

E-commerce, channels

While wholesale continues to be one of the top channels, supported by 43%, that’s down from 55% last year. This year, 47% serviced retail stores, up sharply from 28% last year. Those focused purely on e-commerce is down to 25% this year compared to 36% in 2023; while omnichannel is cited by 25% this year as well, down by 5% compared to last year. Micro-fulfillment delivery to customers stayed at 19% this year.

When we asked about how channels are being fulfilled, self-distributed from one main DC is cited by 51%, up from 32% in 2023. Using a third-party logistics (3PL) provider for e-commerce and internal DCs for other channels decreased a bit: from 14% last year, to just 4% this year, though using a 3PL for all channels, at 9%, did tick up by 4% compared to last year.

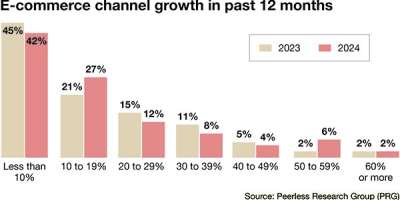

Those saying e-commerce grew 60% or more also rose from 2% last year to 9% this year. Of course, e-commerce activity can influence many things, from order picking strategies to design for the DC network or the need to tap 3PLs.

While e-commerce growth patterns stayed fairly similar year over year, this year, 15% say e-commerce grew between 19% to 20%, compared to 12% last year. Additionally, 11% report e-commerce growth of between 30% to 39%, up from 8% last year.

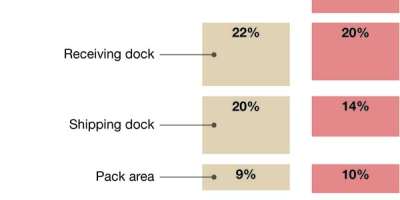

The “most congested” area of the warehouse this year again was storage, with a 37% response, up from 30% last year, followed by receiving (20%) and shipping (14%).

When asked if operations were expanding in terms of factors like SKUs or people over the next 12 months, a net of 84% plan to expand in some way, up from 83% last year.

Compared to last year, 27% plan to expand on number of SKUs, up from 22% in 2023, while 23% plan to expand the number of buildings (compared to 17% last year) and 11% anticipate taller buildings (up from 7%). Only 14% plan to add more people, down from 37% last year.

Inventory & storage

The survey’s findings on inventory reflect just how hard it is to optimize inventory levels and SKU mixes today, even a few years out from the massive disruptions related to the pandemic. For example, while annual inventory turns trended upward last year, rising to 8.2 turns per year on average, this year, that crept back to 6.5 turns per year, which is the lowest average annualized turn rate over the past four years.

Meanwhile, the average number of SKUs among respondents was 7,790 SKUs this year, down from 8,494 last year, and 10,371 in 2022, making three successive years of smaller SKU counts.

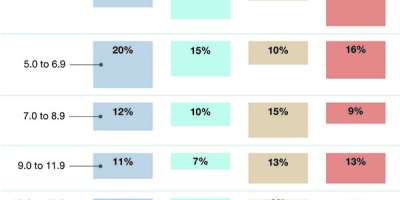

Average peak warehouse space utilization fell from 78.5% last year to 73.2% in 2024. This year, 21% say they’re between 85% to 94% full during peak, down from a quarter of respondents last year.

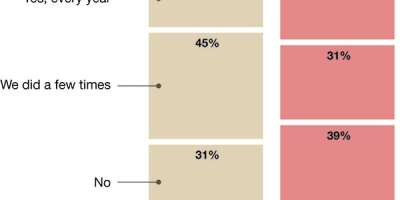

The survey also asks if, within the past five years, the operation leased space during peak times. This year, 39% reported they did not lease additional space at peak, compared to 31% last year; 31% said they did a few times, compared to 45% last year; and 31% reported yes, they do lease additional space during peak every year, compared to 24% who said that last year.

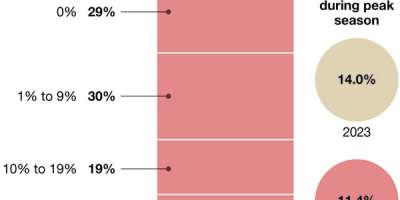

When it comes to the percentage of workforce who are temps during peak, the average this year fell to 11.4%, from 14% in 2023 and 20% in 2022. Only 4% of respondents this year said 50% or more of the workforce consisted of temporary labor during peak volume periods.

As for alternative resources for finding temporary workers, this year, temp agencies led the way at 38%; staffing agencies are used by 32%; 22% used contract firms; 16% make use of on-call workers; 14% use GIG worker resources; and 10% use other methods. Last year, GIG worker platforms were used by 13%, so use of this method did increase by 1%.

On our question about annualized employee turnover rate, this year, 49% say it was 15% or less; but close to a third (31%) deal with a turnover rate of between 16% to 30%.

In terms of retention methods (multiple answers permitted), the leading practice this year is cross training, cited by 31%, followed by bonus/recognition programs, at 25%, and increase base pay, at 17%. Last year, the most often cited method was increased base pay, named by 27%.

Technology progress

This year’s survey points to larger capex budgets, as well as broader adoption of software and automation technologies for everything from WMS, to slotting, to sortation.

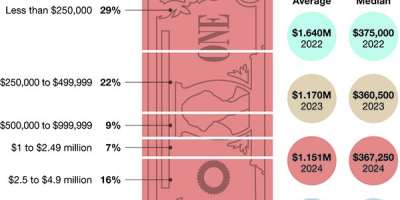

For 2024, respondents had an average capex projection of $1.8 million for warehousing equipment and technology, up from $1.15 million last year. The median rose too, from $367,250 last year, to $375,00 this year. While 19% say their estimated budget would be less than $250,000, 4% have a budget topping $10 million, and a combined 29% have budgets ranging from $1 million to $9.99 million.

Other positive signs of technology adoption this year include the following.

- Use of WMS software reached 93%. This year, ERP-based WMS is the most cited type of WMS, followed by a legacy system, with use of best-of-breed WMS holding steady at 13%.

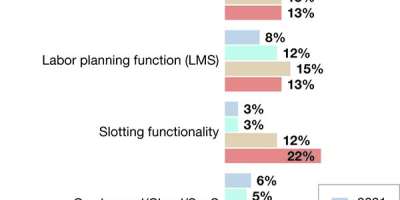

- Use of slotting functionality jumped from 12% last year, to 22% this year. Use of labor management systems (LMS) functionality stayed pretty steady, at 13%, down 2% from last year.

- For 2024, 13% said they use some type warehouse execution system (WES) or warehouse control system (WCS), up from 8% last year. Such systems are used to control and orchestrate automation.

- Use of paper-based picking methods fell to 44% this year, from 56% the year before, and 53% back in 2022. Use of pick-to-light systems edged up 3% this year to reach 16%.

- When we asked about materials handling systems in use, use of sorters increased to 23% from 13% last year. Another growth segment was palletizers, up from 16% last year to 24% this year. Use of mobile robots and industrial robotic arms trended down, but still exceeded 10%.

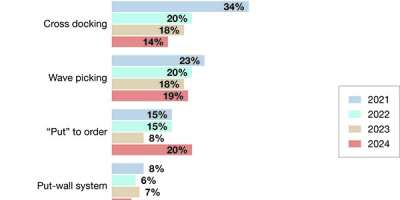

- When asked about order filling techniques, there was increasing use of batching, zone picking, and order waving methods commonly facilitated by WMS or WES software. For example, use of batch picking rose to 44% this year, from 39% last year. We also asked about waveless picking logic this year, with 14% saying they make use of it.

With WMS used so widely, it’s no surprise that a majority of respondents report an automated means of data collection. This year, 56% say they use automated data collection via WMS, up from 51% in 2023. Use of manual data collection approaches fell, from 51% last year to 40% this year.

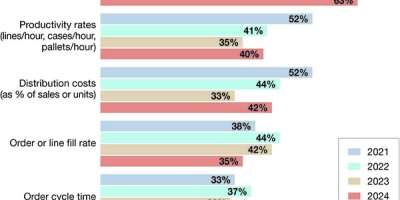

Overall, this year, 86% reported that they use productivity metrics of some type, up 2% from 84% last year. Commonly used metrics include units/piece per hour, leveraged by 46%, from 29% the year before; and orders per hour, used by 34% this year, down from 48% last year.

This year, 96% say they use metrics to manage DC operations, up from a net of 95% using some type of metrics. Types of metrics with a stronger response this year include inventory accuracy, in use by 70%, up from 68%; distribution costs as a percentage of sales, used by 42% this year (up from 33%), and on-time shipping, used by 63% this year, up by 5% over last year, and marking three straight years of growth for use of this metric. Thirty-three percent are tracking perfect order rate, down a bit from 35% last year.

While there’s tactical value to using systems like WMS or WES to direct work for associates or to manage order release to automated systems and robotics, Saenz observes that, overall, software and technology provide managers with dashboards and metrics to make better use of data, while also functions like slotting and smart order release in WES/WMS to get away from the inefficiencies of traditional straight-line order picking.

“There are many positive trends at play here, like getting away from paper-based methods and getting more into automated data collection and generation of useful metrics,” says Saenz. “When you combine that with the big bump in the use of WMS, and functions like slotting and WCS/WES, it is just more positive signs from the survey that companies are making greater use of technology and automation.”

Challenges continue

Difficulty in being able to find and retain a qualified hourly workforce has always ranked highly when we ask about top issues impacting DC operations. This year, a couple of other issues ranked higher, though finding and retaining frontline workers is still ranked as important by 34% of respondents, down from 42% last year.

The top issues this year, however, were different. The most cited response is “outdated storage, picking, or material handling equipment,” named by 45%, a 10% increase from last year. Also, 35% say there were problems with insufficient space in the network, or space/storage modifications, down from 44%, but still cited more often than issues with retaining hourly employees.

Additionally, 33% say they have issues attracting and retaining supervisory staff, up from 20% last year. This year, 23% also tell us that they had concerns about adequate SKU weights and dimensions data, up from 13% the previous year. Supply chain disruption concerns grew by 8%. Each year the survey also asks if your supply chain operation has experienced a catastrophic event of some type (including extreme weather like hurricanes, or events like strikes or supplier failures) in the past two years. This year, 86% say they had not experienced a major disruptive event, up from 77% last year.

This year, when we asked if respondents have accurate weight and dim data in their item masters, 60% say yes, up from 58% last year. Additionally, on the question about major issues, 23% say lack of weights and dims was a key issue, up from 13% last year.

“People realize that having accurate weights and dims is important, whether your operation is largely manual or automated,” says Saenz. “A WMS can’t direct activity correctly without knowing what SKUs will fit where.”

As for technology as a whole, the capex budget finding was positive, and so too were other findings, like greater use of batching and zone picking strategies, says Saenz. “Findings like more use of batching logic, and also more use of automated data collection—these are all consistent with greater use of technology.”

Related presentation

SC

MR

More Warehouse Operations

What's Related in Warehouse Operations

Explore

Explore

Topics

Business Management News

- Innovators Netstock, Pickle Robot win NextGen Solution Provider awards

- Bigger trucks versus broken bridges and roads

- From salon to dock door: Repurposing scheduling software for inbound flow

- The biggest barrier to AI in supply chains isn’t technology

- Rebuilding a planning function around the physical world

- Why companies blame the wrong supplier … and miss the real failure

- More Business Management

Latest Business Management Resources

About the Author

Roberto Michel, Editor at Large

Roberto Michel, senior editor for Modern, has covered manufacturing and supply chain management trends since 1996, mainly as a former staff editor and former contributor at Manufacturing Business Technology. He has been a contributor to Modern since 2004. He has worked on numerous show dailies, including at ProMat, the North American Material Handling Logistics show, and National Manufacturing Week. You can reach him at: [email protected].

Follow SCMR on social media.

@SupplyChainManagementReview on Facebook

@SCMR on Twitter

SCMR on Linkedin

Subscribe

Supply Chain Management Review delivers the best industry content.

Editors’ Picks