The closure of the Strait of Hormuz has roiled global energy markets. Diesel fuel is among the most affected, with prices increasing 46% from the first week in February. Though there has been much alarm over the likely economic effect, the impact of higher diesel prices on motor carriers and supply chains will be minimal. Sudden prices swings are disruptive, but U.S. transportation networks can sustain higher diesel prices.

The first question to address is who ultimately pays the higher cost of diesel in trucking markets. The answer is shippers. Whether it is contract markets, where diesel is priced explicitly and separately, or spot markets, where it is not, diesel costs are quickly and entirely passed through. There are three important pieces of evidence for this.

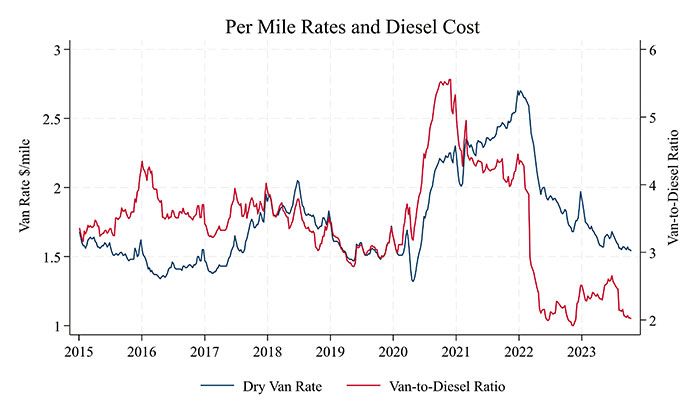

First, we can look at the data on how temporal variation in diesel prices translates to variation in spot market prices. This is shown in figure 1, where diesel prices are translated into dollars per mile, assuming a factor of 6 miles per gallon. Statistical analysis shows that 50% of the change in diesel prices is immediately passed through. Within a week, the pass-through rate hits 100%.

The second piece of evidence on pass through is based on state-level variation in diesel taxes. California has a high tax rate on diesel. Mississippi has one of the lowest diesel tax rates. Other things equal, you would expect truckload rates in California to be higher than those in Mississippi. Research has found exactly this; moreover, the pass-through for these taxes is complete—even over-shifted so that shippers pay a markup.

Third, there is a theoretically compelling argument for full pass-through. The motor carrier industry is extremely competitive, with thousands of motor carriers entering and exiting the market each year. This competition makes profit margins so razor-thin that industry supply is dictated by the cost of service. Shipper demand for freight transportation, on the other hand, is comparatively less sensitive to price. Based on economic theory alone, we expect full pass through. Motor carriers are not in a position to absorb the diesel costs because they would suffer losses and go out of business. While some cargoes may go unshipped during periods of high prices, most freight still must move.

Motor carriers do suffer losses and go out of business all the time. Volatile prices are difficult to manage, especially for smaller motor carriers that do not have dedicated staff of market researchers and price analysts. It takes time for them to adjust to the new reality. Fleet fuel efficiency also matters. High mpg fleets can undercut the less fuel-efficient fleets, so reduce your speed and deploy those boat tails!

These three pieces of evidence paint a compelling picture of an industry that adjusts to fluctuations in fuel prices. While that is reassuring for motor carriers, it does leave a question of the aggregated effects.

Will these cost increases show up in higher consumer prices? You won’t notice it. On average, transportation (all of it) makes up 3-4% of the value added in the country. The items where transportation does account for a significant share of costs (fresh fruits and vegetables, say) make up a small share of household budgets.

Energy prices have long been volatile. Transport markets and supply chains have evolved to be robust to the inevitable price swings.

About authors

Andrew Balthrop is an assistant professor of supply chain management at the University of Tennessee, Knoxville, where he teaches logistics operations management. His research focuses on safety and environmental policy in the trucking industry.

Timothy Fitzgerald is an associate professor of economics at Baker School of Public Policy and Public Affairs at the University of Tennessee, Knoxville where he teaches energy economics. He served as a senior economist on the White House Council of Economic Advisors, 2017-2018. His research focuses on natural resource and energy economics.

SC

MR

More Trucking Costs

Explore

Explore

Topics

Procurement & Sourcing News

- Why companies blame the wrong supplier … and miss the real failure

- NextGen Supply Chain Conference unveils agenda focused on AI, execution and the future of leadership

- From fragmented negotiations to coordinated negotiation performance: an AI-enabled approach

- Supply chain resilience isn’t a data problem; it’s a judgment problem

- Why your supply chain risk management plan will fail

- When component verification becomes operational

- More Procurement & Sourcing

Latest Procurement & Sourcing Resources

Subscribe

Supply Chain Management Review delivers the best industry content.

Editors’ Picks