Sorry, but your login has failed. Please recheck your login information and resubmit. If your subscription has expired, renew here.

January-February 2026

The January 2026 issue of Supply Chain Management Review explores how rapid advances in autonomous trucking, AI-driven optimization, and workforce development are redefining what it means to lead a modern supply chain. As autonomy, data intelligence, and new operating models reshape logistics networks, supply chain managers must rethink how they orchestrate freight, develop talent, manage suppliers, and design resilient operations. Inside, readers will find practical frameworks for scaling autonomous freight management, diagnosing fragile supply chains, uncovering hidden cost drivers, strengthening frontline education programs, and overcoming the… Browse this issue archive.Need Help? Contact customer service 1-508-503-1313 More options

This is my annual update on oil that began with my first Insights column: “Is your supply chain addicted to oil?” (January/February 2007). Since, I’ve focused on the price of oil because freight costs are a sizable (and controllable) portion of supply chain costs. Also, because it appeared that oil prices would rise over time, it was obvious that supply chains would have to be more energy efficient and less dependent on oil. Initially, the tagline was “supply chains needed to slow down” because highly responsive chains were energy inefficient. Furthermore, once there were climate concerns, oil got a “dirty name”—as a polluting CO2 fuel—that became another important reason to squeeze oil out of supply chains.

SC

MR

Sorry, but your login has failed. Please recheck your login information and resubmit. If your subscription has expired, renew here.

January-February 2026

The January 2026 issue of Supply Chain Management Review explores how rapid advances in autonomous trucking, AI-driven optimization, and workforce development are redefining what it means to lead a modern supply… Browse this issue archive. Access your online digital edition. Download a PDF file of the January-February 2026 issue.This is my annual update on oil that began with my first Insights column: “Is your supply chain addicted to oil?” (January/February 2007). Since, I’ve focused on the price of oil because freight costs are a sizable (and controllable) portion of supply chain costs. Also, because it appeared that oil prices would rise over time, it was obvious that supply chains would have to be more energy efficient and less dependent on oil. Initially, the tagline was “supply chains needed to slow down” because highly responsive chains were energy inefficient. Furthermore, once there were climate concerns, oil got a “dirty name”—as a polluting CO2 fuel—that became another important reason to squeeze oil out of supply chains.

Update recap

The titles of my last 5 updates tell most of the story of the recent past.

1. “Oil Update: Still need fracking?” (January/February 2021)

2. “Oil Update: Where’s the global energy plan?” (January/February 2022)

3. “Oil Update: We need security plans from policymakers” (March/April 2023)

4. “Oil Update: The same, for now” (January/February 2024)

5. “Oil Update: Price stability, climate change uncertainties” (January/February 2025)

Over the past several decades, shale fracking in the U.S. has played a major role in moving the oil markets away from the too-often political whims of OPEC and other major oil-exporting countries—including the rogue state of Russia. Fracking became a stabilizing factor in moving the oil market closer to a free market, largely based on supply versus demand principles. While pricing did not grow as fast as expected, it was more volatile and reacted to major economic crashes, wars, and the COVID-19 pandemic. These events caused either demand or supply to significantly change and with that, oil prices as well.

As can be noted from the titles above, climate change initiatives have dominated news cycles. Especially since Russia invaded Ukraine in early 2022. World policymakers realized that plans to primarily reduce the world’s reliance on fossil fuels with renewal energy sources like wind and solar were insufficient. There needed to be three coordinated and balanced plans to achieve: 1) energy security, 2) economic security, and 3) climate security. Climate security alone was not enough, as the first two plans would deal with today’s important issues while climate security focuses on 2050 and beyond.

Climate change talks became unproductive

The U.S. signed the Paris Climate Accords treaty, which covers climate change mitigation, adaptation, and finance, in 2016. It was negotiated by 196 parties at the 2015 United Nations Climate Change Conference and entered into force in November 2016. There appeared to be a mutual global strategy to move away from fossil fuels and replace them with renewables and other CO2 non-polluting energy sources in the long term. Goals were established to reach net zero by the middle of the 21st century

and keep the rise in global surface temperature to no more than 1.5 deg. C above pre-industrial levels. Also, emissions needed to be cut by roughly 50% by 2030. These turned out to be unrealistic goals for a variety of reasons.

As I write this column, the COP30 climate negotiations focused on meeting 2030 goals ended. A Boston Globe article (Nov. 23, 2025) summarized the results in an article titled: “Climate talks end with weak resolution” and subtitled “COP30 seen as insufficient from the outset.” Evidently, the negotiations ended “with a watered-down resolution that made no direct mention of fossil fuels, the main driver of global warming.” More importantly no specific plans for reducing fossil fuel emissions.

An article published by The New York Times (Sept. 17, 2025) titled “It Isn’t Just the U.S. The Whole World Has Soured on Climate Politics,” chronicled the growing disillusionment with climate change politics. Some telling excerpts are:

- “The world hasn’t actually abandoned green energy, with global renewal rollout still accelerating and investment doubling.”

- “But climate politics is in undeniable withdrawal, and far from ushering in a new era of cooperative global solidarity.”

- “Polls show that voters don’t actually prioritize decarbonization and, crucially, aren’t willing to pay much to bring it about.”

- “Progressives long believed that climate politics was a kind of tug of war, in which tugging harder would pull many on the other side over the line into grudging support … But it also looks a bit as if they pulled so hard they collapsed in disarray.”

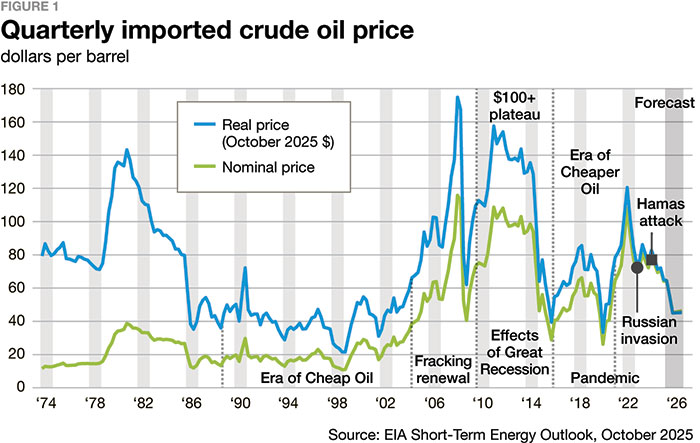

A 50-year history of oil pricing

In each oil update I’ve shown Figure 1, an updated historical chart depicting real quarterly imported crude oil prices since 1974. The chart shows various pricing levels through time. After the era of cheap oil ended with rising prices, the first signs of cheaper oil appeared as a precipitous drop, the result of the Great Recession of 2008, which drastically depressed worldwide economies and the demand for oil. This was followed by a three-plus-year period termed the “$100+ plateau” before receding to cheaper oil. The $100+ plateau ominously looms in the rearview mirror as a reminder of what could happen if worldwide economic and supply conditions reach the robust levels seen prior to the recession.

Over the period of higher oil prices, U.S. oil fracking operations came online because the prices were high enough to justify the investment. U.S. frackers innovated and reached a point where operations were flexible enough to easily turn on and off as oil prices move up and down. The fracking industry made the United States the world’s top oil supplier and a net exporter. In addition, fracking output caused a worldwide oversupply of oil that brought back the era of cheap oil. However, as discussed in my 2021 update, oil prices dropped to cheap oil levels when the pandemic began—prices not seen since around 2004. I questioned whether fracking was still economically justified. As seen from Figure 1, the Russian invasion triggered a spike in prices. However, it was short-lived, peaking to over the $100+ plateau for only one quarter and back down to cheaper oil—hovering around $70 to $80/barrel. It has largely remained there since last year’s update. It seems that the $100/barrel of oil level is approaching a ceiling as this is the level at which frackers start to show an interest—driving up supply.

Recent news regarding climate initiatives

Generally, the world is struggling to meet COP’s emission targets mainly because the thirst for energy, and in particular fossil fuels, has not subsided. Population and economic growth require growing energy use. According to a 2024 United Nation’s forecast, the world population will peak in 2084 at just under 10.3 billion from about 8.2 billion today. However, despite zealous advocates pushing policymakers to develop practical plans to replace fossil fuels with renewables, no plan has yet been agreed upon. Many thought that replacing coal and oil use with more natural gas (as a bridge fuel), was one key element. In addition, wind and solar renewable sources would be aggressively relied upon, as well as all other non-fossil fuels. However, policymakers need to serve their constituents, and nuclear, by public opinion, was deemed unsafe. Ten years of valuable nuclear development did not happen. Below are some of the policymakers’ less-than-successful initiatives.

- An over reliance on renewables growth. In a Wall Street Journal article (Oct. 8, 2025) titled “U.S. Renewal Energy Growth Outlook Cut,” it stated that the International Energy Agency slashed the growth forecast 50% from its last annual forecast. While solar is doing okay, the weak spot for renewals is in wind because of “permitting delays, supply chain bottlenecks, and rising costs.”

- Promoting just electric vehicles (EVs), rather than hybrids as well. In “U.S. Shift Against Electric Cars Swells into Global Reversal” (WSJ, Oct. 15, 2025), it stated that “AlixPartners now predicts EVs will make up 18% of new vehicle sales by 2030, half of what was expected two years ago.” EVs won’t sell enough until there are enough electric chargers.

- Slow gas pipeline development hampers important (and bridging) natural gas growth. In “Gas Pipeline Projects Face Hurdles” (WSJ May 23, 2025), it states that “Five interstate gas projects were canceled between 2013 and 2021…” In Massachusetts, we have to bring in LNG (liquid natural gas) tankers into small harbors at great expense—because we don’t have enough pipeline capacity.

- Deeming nuclear too risky was misguided. Germany’s former strategy to replace all its nuclear power plants with natural gas from Russia was shown to be a bad strategy when Russia attacked Ukraine. In “Environmentalists Fight for Nuclear Plants” (WSJ, Oct. 10, 2025), the article is subtitled “Some activists [e.g. in Belgium] now see reactors as a source of low-carbon electricity.” In other WSJ articles, similar thoughts were: “UK’s First Nuclear Plant since 1995 Wins Approval” (July 25, 2025); and “US Bets Big on a Revival of Nuclear Power Industry” (Nov. 25, 2025). The later article points out that the U.S.’s “last big nuclear power project came in more than $16 billion over budget and seven years behind schedule.” Plus, it has a chart showing electricity generation by selected sources from 2001 to the present. It shows minimal growth in nuclear, and natural gas basically replacing much of coal’s declines; as well as wind rising to coal’s level.

High-tech firms are now projecting that their AI and future cloud computing operations are going to add substantially to the world’s energy (i.e., electricity) needs. Constellation Energy “announced last year that it would restart the Three Mile Island site of the country’s worst nuclear power accident to help generate electricity for Microsoft, which needs more power to fuel its artificial intelligence business,” according to a WSJ article (Nov. 12, 2025), titled “U.S. Will Give $1 Billion Loan to Restart Three Mile Island.” Google, Amazon, Meta and others are also racing to get more power in order to stay competitive.

Summary

My advice generally stays the same as the past few years. It will always be prudent to reduce the use of carbon-based energy sources by making your supply chains as energy-efficient as possible. However, I expect there will be a substantial growing demand for fossil fuels for some time. As future energy needs appear to be expanding more than needs generated via population growth.

Policymakers are having difficulties weaning their citizens away from fossil fuels. The reality has been that renewable energy, while growing rapidly, has not kept up with the still-growing thirst for fossil fuels. For policymakers, today’s life challenges are getting in the way. They too often need to put climate change policies on the back burner. Generally, in the short term, humans vote for policymakers that focus on the here and now—2050 is too far over the horizon to matter much to today’s voting population.

Meanwhile, don’t expect much significant human action on climate change until Mother Earth strikes back with a highly catastrophic climate change event due to the higher temperatures forecast by scientists. I am optimistic, however, that future supply chain managers will adapt to the new environments, and continue to supply the goods and services needed by the human race (plus robots). After all, it’s what we do for a living.

SC

MR

More Oil Markets

Explore

Explore

Topics

Procurement & Sourcing News

- Why companies blame the wrong supplier … and miss the real failure

- NextGen Supply Chain Conference unveils agenda focused on AI, execution and the future of leadership

- From fragmented negotiations to coordinated negotiation performance: an AI-enabled approach

- Supply chain resilience isn’t a data problem; it’s a judgment problem

- Why your supply chain risk management plan will fail

- When component verification becomes operational

- More Procurement & Sourcing

Latest Procurement & Sourcing Resources

About the Author

Larry Lapide, Research Affiliate

Dr. Lapide is a lecturer at the University of Massachusetts’ Boston Campus and is an MIT Research Affiliate. He received the inaugural Lifetime Achievement in Business Forecasting & Planning Award from the Institute of Business Forecasting & Planning. Dr. Lapide can be reached at: [email protected].

Follow SCMR on social media.

@SupplyChainManagementReview on Facebook

@SCMR on Twitter

SCMR on Linkedin

Subscribe

Supply Chain Management Review delivers the best industry content.

Editors’ Picks