Global trade credit insurer Atradius recently released its annual report on the Asia-Pacific region providing in-depth reviews of each country's performance outlook by industry, and how political and economic situations are playing a role in the current business climate. Major Pacific Rim players include: India, Indonesia, Japan, Malaysia, The Philippines, Singapore, South Korea, Taiwan, Thailand and Vietnam.

But as usual, it is China which generates most scrutiny by global supply chain managers.

Overall, the political situation is stable, say Atradius anlysts, with the Chinese Communist Party (CCP) firmly in power. President Xi Jinping has consolidated his power within the CCP at the October 2017 party congress, and is seen as the most powerful Chinese leader since Deng Xiaoping.

The authorities are expected to proceed with an economic policy course characterized by stability and a gradual pace of changes and reforms. In the short term the focus is on reforming state-owned enterprises (SOEs) and the financial sector, on deleveraging indebted local governments and SOEs and on combatting corruption.

Furthermore, China is increasing its international influence and power projection, e.g. with large direct investments in a range of countries in Asia and Africa (mainly under the umbrella of the “Belt and Road” initiative) and a more assertive stance in its territorial claims in the South China Sea and the conflict over the Senkaku/ Diaoyu islands with Japan. The strengthening of China's geopolitical clout leads to balancing efforts by the U.S., Japan and India.

Despite better than expected economic growth in 2017, business insolvencies in China are expected to increase further in 2018. Companies face tighter lending conditions while the economic structure is changing with a rebalancing towards services and consumption.

Analysts contend that this will inevitably lead to shrinking business opportunities for sectors such as steel, metals, shipping and mining. The situation is exacerbated by the fact that excess capacity and high indebtedness remain an issue in those industries.

While listed and state-owned businesses still benefit from stronger support from banks and shareholders, more caution is recommended when dealing with small and medium-sized private businesses, as many of them - even those active in better-performing industries - often suffer from limited financing facilities.

Doug Collins, Regional Director, Risk Services, for Atradius, notes that while rising interest rates in the U.S. have traditionally been problematic for emerging market economies, those in the Asia-Pacific Region seem well positioned to manage the situation.

“The major economies in the region, including China, India, Vietnam, Indonesia, and the Philippines, carry substantial foreign reserves or generate robust export volumes in relation to foreign-denominated debt, thereby cushioning them from the impact of higher U.S. rates,” he says.

According to Collins, supply chain managers should keep their guard up before going “all in” with their sourcing strategies.

“While overall the growth story in Asia-Pacific continues, with India assuming leadership from China in terms of GDP growth, some pitfalls remain. We expect an increase in bankruptcies in China among medium to small companies,” he says.

In addition, sectors such as aluminum, cement, coal construction, and steel are suffering from over-capacity in China, with heavily indebted players vulnerable to default, even before considering the potential impact of U.S. tariffs and any subsequent trade disruptions.

“High corporate debt is a risk for India as well, with non-performing loans to the corporate sector pressuring the Indian banking sector, which could be a precursor to higher corporate defaults,” says Collins. “For supply chain managers, it is important to understand the dynamics within each market are different, and to understand how local conditions can impact payment risk.”

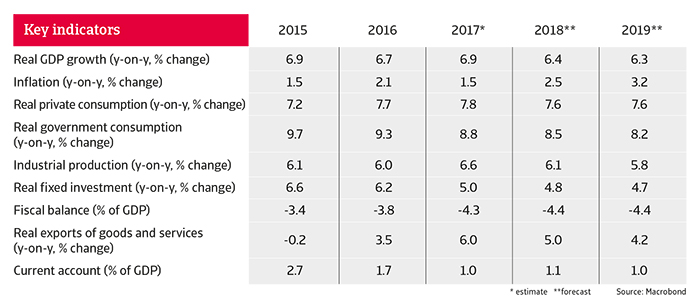

Chinese Key Indicators:

Getting back to China, risk experts observe that its economic expansion of 6.9% in 2017 was the first year of (modest) annual GDP growth acceleration since 2010. Exports showed a strong recovery and household consumption remained steady while investment spending bottomed out.

“In 2018 China's economy is expected to grow more than 6% as external demand should remain strong. Domestic demand is expected to cool down somewhat due to tighter lending conditions,” say Atradius analysts.

As a consequence of economic rebalancing – a transition away from export-oriented investments towards more consumption-led growth, China's growth rate is expected to see a gradual, but substantial slowdown reaching a level of about 5.2% in 2022.

SC

MR

Latest Supply Chain News

- From salon to dock door: Repurposing scheduling software for inbound flow

- The biggest barrier to AI in supply chains isn’t technology

- Rebuilding a planning function around the physical world

- Why companies blame the wrong supplier … and miss the real failure

- NextGen Supply Chain Conference unveils agenda focused on AI, execution and the future of leadership

- More News

Latest Podcast

Explore

Explore

Business Management News

- Why companies blame the wrong supplier … and miss the real failure

- NextGen Supply Chain Conference unveils agenda focused on AI, execution and the future of leadership

- Supply chain resilience isn’t a data problem; it’s a judgment problem

- Beyond the hype: Building flexible and scalable supply chains in a VUCA world

- Why your supply chain risk management plan will fail

- What options do you really have? Shaping the supply chain resilience funnel

- More Business Management

Latest Business Management Resources

About the Author

Patrick Burnson, Executive Editor

Patrick is a widely-published writer and editor specializing in international trade, global logistics, and supply chain management. He is based in San Francisco, where he provides a Pacific Rim perspective on industry trends and forecasts. He may be reached at his downtown office: [email protected].

Follow SCMR on social media.

@SupplyChainManagementReview on Facebook

@SCMR on Twitter

SCMR on Linkedin

Subscribe

Supply Chain Management Review delivers the best industry content.

Editors’ Picks