Sorry, but your login has failed. Please recheck your login information and resubmit. If your subscription has expired, renew here.

July-August 2026

The July issue of Supply Chain Management Review explores how organizations are preparing for the future through workforce development, AI adoption, leadership education, and supply chain resilience. Features examine closing the skills gap, building AI-enabled teams, strengthening supplier networks, and developing practical strategies for navigating disruption in an increasingly complex global marketplace. Browse this issue archive.Need Help? Contact customer service 1-508-503-1313 More options

When a trade restriction is announced or a hyperscaler revises its AI spending guidance, the semiconductor industry’s real response was already set in motion years earlier. A leading-edge fabrication plant costs over $20 billion and takes three to four years from investment decision to first production wafer. The specialized equipment inside, lithography systems that cost $200 million to $400 million each, comes from a handful of global suppliers with lead times of 12 to 24 months. Once the factory is operational, each wafer moves through hundreds of process steps over four to six months before becoming finished chips. Capacity decisions made today will not produce chips until 2029 or 2030. But the demand these fabs must serve, and the policy environment they operate under, can shift in a single quarter.

SC

MR

Sorry, but your login has failed. Please recheck your login information and resubmit. If your subscription has expired, renew here.

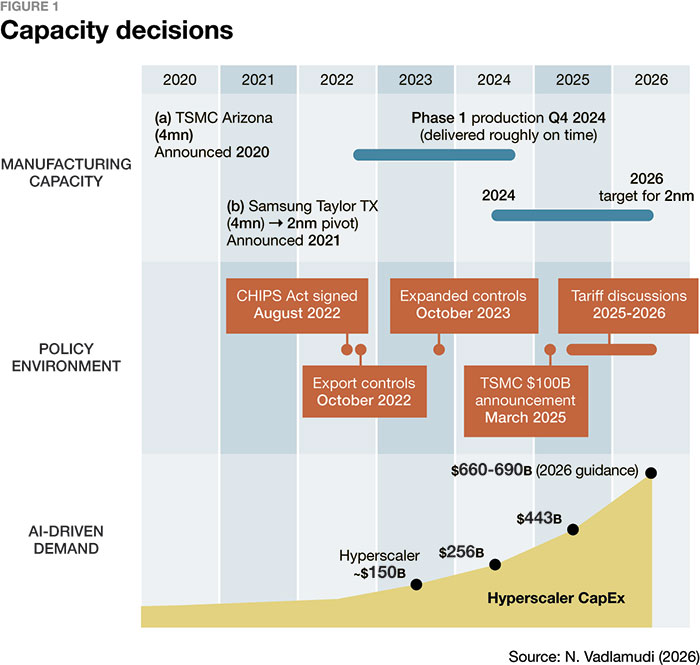

When a trade restriction is announced or a hyperscaler revises its AI spending guidance, the semiconductor industry’s real response was already set in motion years earlier. A leading-edge fabrication plant costs over $20 billion and takes three to four years from investment decision to first production wafer. The specialized equipment inside, lithography systems that cost $200 million to $400 million each, comes from a handful of global suppliers with lead times of 12 to 24 months. Once the factory is operational, each wafer moves through hundreds of process steps over four to six months before becoming finished chips. Capacity decisions made today will not produce chips until 2029 or 2030. But the demand these fabs must serve, and the policy environment they operate under, can shift in a single quarter (see Figure 1).

The structural tension in semiconductors is defined by three colliding timelines. First is manufacturing capacity, where fabs costing $20 billion or more are physics-constrained and irreversible once committed. The contrast between announced timelines and actual delivery is stark: TSMC broke ground on its Arizona fab in 2021 and began 4nm production in late 2024, roughly on schedule. Samsung announced its Taylor, Texas, fab in 2021 for 2024 production; it has pivoted from 4nm to 2nm technology and now targets late 2026 at the earliest. Second is the policy environment, where export controls, CHIPS Act incentives, and tariff shifts can occur within weeks. Third is AI-driven demand, where the global semiconductor market is projected to reach $975 billion by 2026 according to WSTS, on quarterly earnings cycles with annual spending swings exceeding 50%. This tension between long capital commitments and short-cycle volatility exists across capital-intensive industries, but no sector makes it as visible, or as consequential, as semiconductors.

Why lead times cannot be compressed

The semiconductor capacity pipeline is inherently incompressible because it is bound by supplier concentration, the physics of yield learning, and serial qualification requirements. Capital can be deployed quickly. Converting that capital into qualified, high-volume silicon follows a rigid chronological path that resists acceleration.

Supplier concentration and tool lead times. The most significant bottleneck is the extreme concentration of the upstream equipment supply chain. EUV lithography systems, required for any chip at 7nm or below, come from exactly one company: ASML of the Netherlands. ASML shipped 48 EUV systems globally in 2025 and reported full-year revenue of approximately $39 billion. A standard EUV scanner costs approximately $200 million, while the latest High-NA variant, needed for sub-2nm nodes, costs $370 million to $400 million. With a single supplier producing fewer than 50 systems per year for an entire global industry, delivery slots are committed years ahead. There is no expedited option because there is no alternative supplier. Leading-edge deposition and etch equipment comes from a similarly concentrated group: Applied Materials, Lam Research, and Tokyo Electron collectively determine the pace at which new semiconductor capacity can be equipped.

The physics of yield learning. A new fab typically starts producing chips at yields of 30% to 50%. Reaching competitive yields above 80% requires 18 to 24 months of systematic process optimization: identifying defect sources across hundreds of sequential process steps, adjusting parameters, and qualifying materials. Each learning cycle takes weeks because the wafer production cycle itself runs four to six months from bare silicon to finished die. Rushing process qualification does not produce faster results; it produces defective chips.

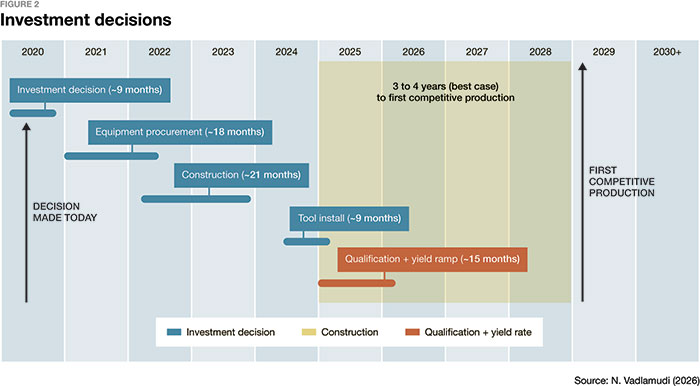

Serial customer qualification. Even after a fab demonstrates stable, high-yield production, customers require an independent qualification process. Automotive-grade chips must meet AEC-Q100 reliability standards. Defense and aerospace components require DMEA accreditation. Hyperscaler customers run proprietary validation suites. These processes typically take six months to 12 months. The total elapsed time from investment decision to qualified revenue consequently extends to four, five, or more years, as multiple reshoring projects have demonstrated (see Figure 2).

The AI demand shock

The semiconductor industry has managed cyclical demand for decades. PC shipments swing 15% to 20% over two- to three-year cycles. Smartphone demand is relatively predictable. Automotive follows long design cycles. AI accelerator demand operates on a fundamentally different scale.

The hyperscaler spending explosion. The five largest hyperscalers, Amazon, Alphabet, Microsoft, Meta, and Oracle, are projected to spend a combined $660 billion to $690 billion on capital expenditure in 2026, nearly tripling from approximately $256 billion in 2024. Amazon alone committed to approximately $200 billion. Alphabet guided $175 billion to $185 billion. Microsoft is on pace for approximately $145 billion. Each of the four largest hyperscalers will individually exceed $100 billion in annual infrastructure spending. Goldman Sachs projects total hyperscaler CapEx from 2025 through 2027 will reach nearly $1.4 trillion, almost triple the approximately $485 billion spent from 2022 through 2024. Approximately 75% of this spending is directed at AI infrastructure.

The memory bottleneck. The demand pressure extends beyond logic chips. High-bandwidth memory (HBM), essential for AI accelerators, is sold out through 2026 across all three major manufacturers. Micron CEO Sanjay Mehrotra confirmed that HBM capacity is fully committed under multi-year agreements. The constraint is structural: each gigabyte of HBM consumes roughly four times the wafer capacity of standard DRAM, according to TrendForce. This has led to projections of a 171% year-over-year price increase for conventional DRAM in 2026 as consumer-grade supply is reallocated for AI production. Advanced packaging capacity, particularly TSMC’s CoWoS platform, remains similarly constrained. AI demand does not simply compete for fab capacity; it cascades through memory, packaging, and substrate supply

chains simultaneously.

A two-front planning challenge. What makes the current environment unprecedented is that demand volatility and policy volatility are hitting simultaneously. An export control change does not just restrict where chips are sold; it redirects global demand in real time. A subsidy program does not just fund new fabs; it reshapes competitive geography, potentially stranding investments in regions that lose their policy advantage. The CHIPS Act and EU Chips Act together are channeling over $100 billion in public funds into reshaping where semiconductors are manufactured, while tariffs and export controls can shift the competitive calculus in weeks.

The planning question has shifted from “how much capacity do we need?” to “how much capacity do we need, where, for whom, under which regulatory regime, and what happens if any of those assumptions change before the fab is operational?” This combinatorial explosion of scenarios is precisely why traditional deterministic planning fails. The semiconductor capacity decision is no longer an optimization problem with a single best answer. It is a portfolio problem requiring robustness across a range of plausible futures.

How semiconductor companies are adapting

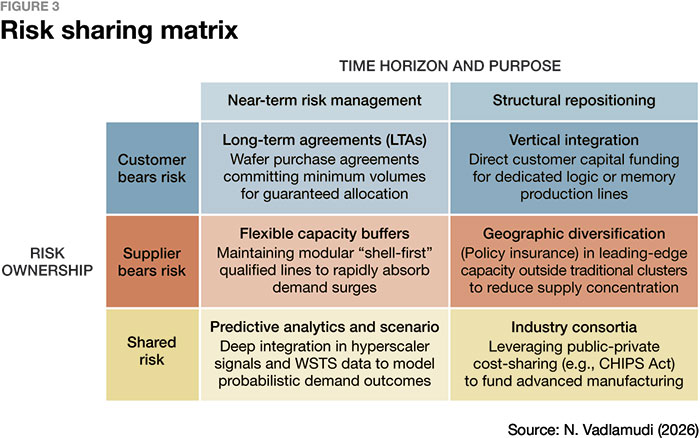

Semiconductor companies cannot eliminate the temporal mismatch between multi-year fab builds and quarterly demand cycles. What they can do is distribute their risks more intelligently. The adaptation strategies now standard in the industry map onto two dimensions: time horizon (near-term operational adjustments versus structural repositioning) and risk ownership (who bears the cost when assumptions prove wrong).

The shift to long-term agreements. Before the 2020 to 2023 shortages, much of the foundry market operated on relatively flexible, shorter-term commitments. That era is over. Take-or-pay LTAs with multi-year volume and pricing commitments have become the standard mechanism for securing leading-edge capacity. NVIDIA, AMD, Apple, and Qualcomm have all publicly disclosed multi-year TSMC commitments. Micron’s CEO Sanjay Mehrotra has described the company’s HBM supply agreements as “multi-year in nature,” fundamentally different from the transactional contracts of the past. The strategic implication: companies that locked in capacity early now hold durable advantages. For customers, LTAs are no longer a procurement decision; they are a board-level strategic commitment that shapes product roadmaps years into the future.

Geographic diversification as policy insurance. No geography is immune to policy risk. TSMC’s expansion to Arizona (now totaling $165 billion across six planned fabs), Kumamoto in Japan, and Dresden in Germany reflects explicit “policy insurance.” Research by BCG and the SIA found that a new fab in the U.S. costs approximately 30% more to operate than equivalent capacity in Asia. Companies are paying this premium because concentrated exposure to any single government’s decisions is now considered unacceptable strategic risk. Intel’s Fab 52 in Chandler, Arizona, reached Intel 18A high-volume manufacturing in late 2025, adding US-based 2nm-class capacity to a global advanced-node supply base that has historically concentrated in Asia.

Modular and flexible fab design. To manage the risk of building a fab that may face different demand by the time it is operational, suppliers are increasingly adopting modular construction, building the shell and cleanroom infrastructure first, then phasing equipment installation as demand signals clarify. Within the fab, tool fungibility adds another layer of flexibility. While lithography systems are largely node-specific, much of the equipment base, deposition, etch, and metrology tools can serve multiple process nodes with recipe changes. A fab designed for one node can partially reallocate capacity to adjacent nodes as demand shifts. This does not eliminate the temporal mismatch, but it reduces the portion of the commitment that is irreversible.

Predictive analytics and scenario planning. Traditional capacity planning used deterministic models: forecast demand, optimize the production plan, and commit. This approach fails when forecast horizons of three to four years collide with quarterly demand revisions of 30% to 50%. Leading semiconductor companies are shifting to probabilistic approaches that model ranges of outcomes. Multi-signal demand forecasting integrates macroeconomic indicators, industry-specific metrics (WSTS shipment data, equipment booking trends, fab utilization rates), and customer-level signals (hyperscaler earnings guidance, CapEx revisions) to reduce forecast error, particularly during regime changes when historical patterns break down. Emerging signals such as AI inference token generation growth rates are providing capacity planners with earlier visibility into demand trajectories.

The honest limitation: even sophisticated analytics cannot predict export control decisions or the trajectory of AI adoption. What it can do is narrow the range of uncertainty that must be managed through the other strategies. Analytics does not replace risk-sharing; it right-sizes the cost of managing uncertainty.

Beyond semiconductors: A framework for any capital-intensive supply chain

The semiconductor industry’s extreme capital intensity and lead times forced it to develop these adaptation strategies first. But the underlying dynamics are not unique to chips. Two other industries illustrate how the same framework applies.

Aerospace: The geared turbofan crisis. Pratt and Whitney’s PW1000G geared turbofan engine, which powers approximately half of all Airbus A320neo-family jets, has been subject to a massive recall since 2023 due to a powder-metal defect in turbine disc forgings. As of late 2025, approximately 835 GTF-powered aircraft were grounded according to Cirium fleet data, roughly one-third of the GTF-powered Airbus fleet. Maintenance turnaround times ballooned from 60 days to over 300 days. RTX expects recovery to extend through the end of the decade. In February 2026, RTX announced a $200 million investment to install a seventh isothermal forging press, aimed at increasing critical engine component output by 30% by 2028. The constraint is not funding; it is the physics of metallurgical inspection and the concentration of qualified manufacturing capacity.

Energy: The power transformer shortage. The utility sector faces lead times for large power transformers of 128 weeks (approximately 2.5 years), while generator step-up transformers reach 144 weeks. Demand has surged more than 100% since 2019, driven by AI data centers, EV charging infrastructure, and aging grid replacement. Wood Mackenzie projects a 30% supply deficit for power transformers. The DOE’s $1.9 billion SPARK program represents public-private cost-sharing for grid modernization. Hitachi Energy’s $1 billion manufacturing investment, including a $457 million transformer factory in Virginia, aims to reduce U.S. dependence on imported units. Despite billions in investment, supply deficits are projected to persist into the 2030s because production remains constrained by a global shortage of grain-oriented electrical steel.

Closing. The temporal mismatch between long capital commitments and short-cycle volatility is not an anomaly of semiconductor manufacturing. It is becoming the defining challenge of capital-intensive supply chains, intensified by AI-driven demand creating unprecedented volatility, policy intervention reshaping competitive geography faster than manufacturing can respond, and concentrated supply bases creating structural bottlenecks resistant to brute-force investment.

There is no solution that eliminates this mismatch. The goal is not to resolve the tension but to manage it through risk-sharing mechanisms, robust capacity configurations, and planning processes that model uncertainty rather than assuming it away. The semiconductor industry developed these approaches first because it had no choice. The rest of manufacturing would be wise to adopt them before the same forces arrive at their door.

About the author

Nikhil Vishnu Vadlamudi works in semiconductor operations with experience spanning the value chain at Applied Materials, AMD, and Intel. He brings a practitioner’s perspective to foundry operations, capacity planning, demand forecasting, and S&OP. His work focuses on AI/ML-driven optimization of semiconductor manufacturing operations and strategic decision-making,

bridging process technology, supply chain dynamics, and the operational realities of scaling semiconductor production.

SC

MR

More Risk Management

- Supply chain resilience isn’t a data problem; it’s a judgment problem

- Why your supply chain risk management plan will fail

- Lead time economics: What semiconductor supply chains reveal about strategic planning

- Chokepoints need the ‘Theory of Constraints’

- The hidden supply chain risk no dashboard shows

- More Risk Management

What's Related in Risk Management

Explore

Explore

Topics

Procurement & Sourcing News

- Innovators Netstock, Pickle Robot win NextGen Solution Provider awards

- From salon to dock door: Repurposing scheduling software for inbound flow

- The biggest barrier to AI in supply chains isn’t technology

- Rebuilding a planning function around the physical world

- Why companies blame the wrong supplier … and miss the real failure

- NextGen Supply Chain Conference unveils agenda focused on AI, execution and the future of leadership

- More Procurement & Sourcing

Latest Procurement & Sourcing Resources

Subscribe

Supply Chain Management Review delivers the best industry content.

Editors’ Picks