Sorry, but your login has failed. Please recheck your login information and resubmit. If your subscription has expired, renew here.

November 2019

We hear a lot about emerging technologies like artificial intelligence, machine learning and robotics. We hear less about one of the enabling technologies that makes the others possible: Browse this issue archive.Need Help? Contact customer service 1-508-503-1313 More options

In last year's “Warehouse and Distribution Center (DC) Operations Survey,” the tight labor market stood out as the overriding challenge for warehouse operations managers. For the 2019 edition, not only did labor scarcity remain the top challenge, but also the results show that respondents are taking action to mitigate the problem.

In fact, this year's respondents report that they're using multiple methods of strengthening their workforces. One of these is increasing pay, which 54% said that they did this year. Other strategies include enhanced training and better benefits.

These struggles to find and retain an effective workforce are being done against a backdrop of continued business growth and the ongoing impact of e-commerce fulfillment activity. For 2019, 42% are involved in e-commerce, and 20% said that they service an omni-channel environment. Other telling data points are outlined below.

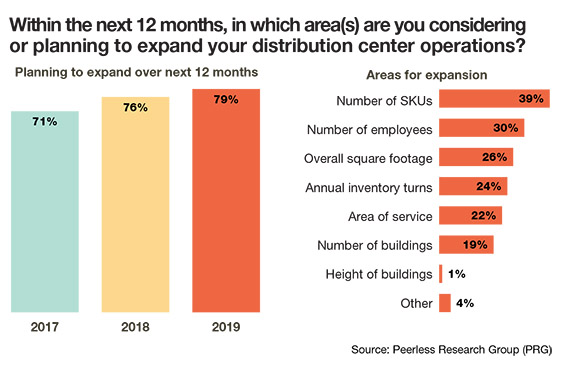

- Business confidence appears solid: When asked if their operation was planning to expand in the next 12 months, 79% said, “yes,” which is 3% higher than last year.

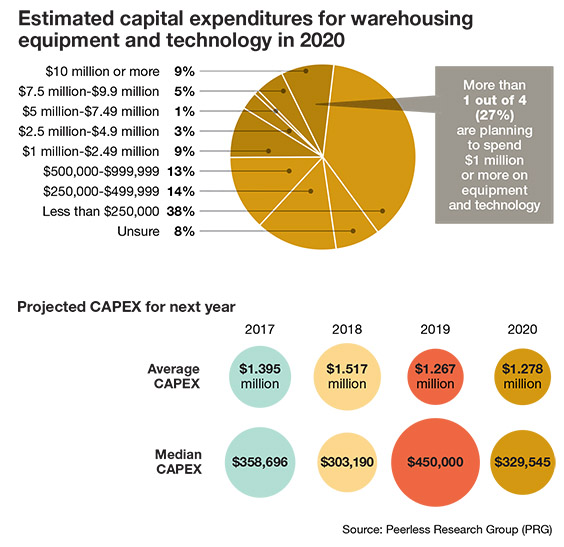

- Capital expenditure (capex) plans remained healthy. The average projected capex for the next year was $1.27 million, nearly identical to last year. While the average respondent was at a smaller operation this year, which likely lowered the median, 9% plan to spend $10 million or more.

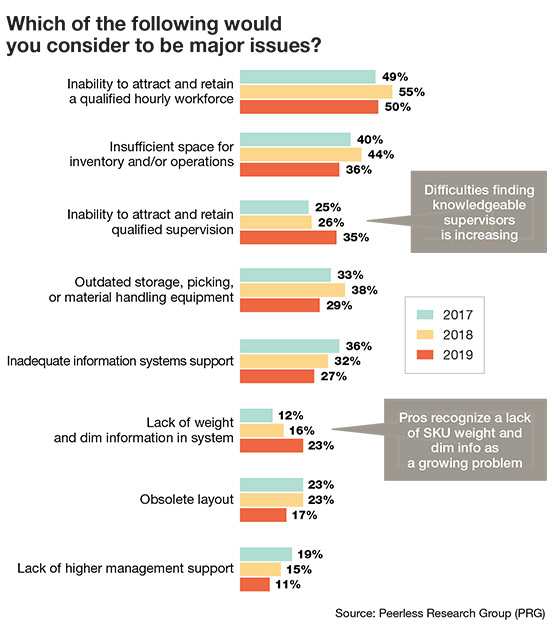

- Inability to attract and retain a qualified hourly workforce was again the leading industry issue, cited by 50% of respondents. This was down a bit from last year, but those concerned about the inability to find good supervisors shot up from 26% last year to 35% this year.

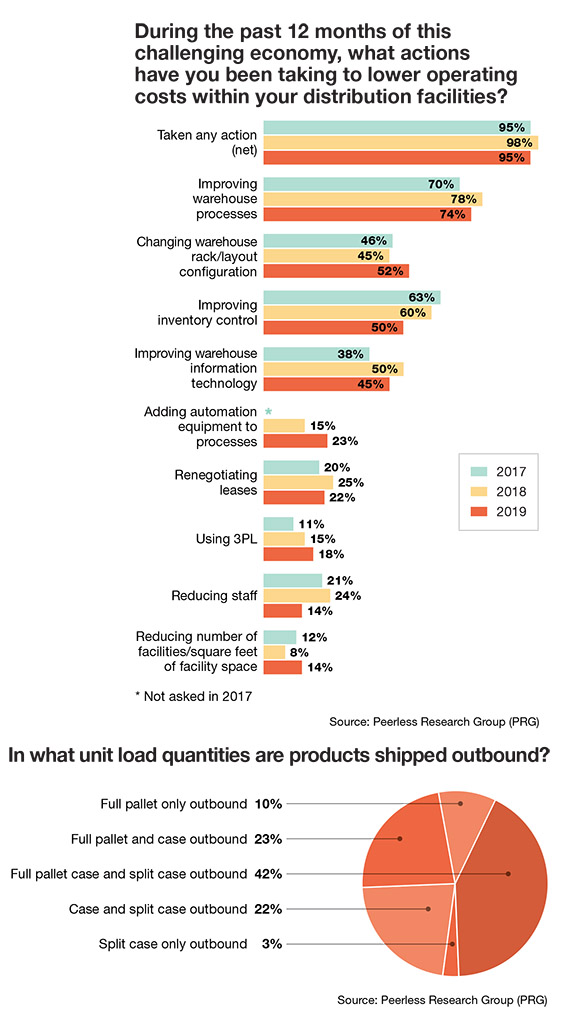

- Responses around technology use were mixed in some regards, but generally pointed toward a continued surge in the willingness to apply automation and software. For example, on a question about actions for managing DC costs, 23% said they were adding automation to contain costs, up from 15% last year.

The survey, conducted annually by Peerless Research Group, drew 146 responses this year from professionals in logistics and warehouse operations across multiple verticals. According to Norm Saenz, Jr., a managing director with St. Onge Company, and Don Derewecki, a senior consultant with St. Onge Company, a supply chain engineering consulting company and our partner for this annual survey, respondents are coping with many areas of change, with a common strategy being the use of more technology.

The survey, conducted annually by Peerless Research Group, drew 146 responses this year from professionals in logistics and warehouse operations across multiple verticals. According to Norm Saenz, Jr., a managing director with St. Onge Company, and Don Derewecki, a senior consultant with St. Onge Company, a supply chain engineering consulting company and our partner for this annual survey, respondents are coping with many areas of change, with a common strategy being the use of more technology.

“The pace of change is increasing every year, which needs to be accounted for,” says Derewecki. “This year's survey shows respondents are budgeting for change; they're looking to use more technology and automation; and they are looking to improve their operational processes and controls.”

Saenz agrees that managers responsible for DC operations are focused on ways to find efficiencies to help cope with the impacts of e-commerce growth, and to help mitigate labor scarcity.

“The need to automate more aspects of an operation and find further efficiencies is certainly on the forefront for managers,” says Saenz. “The reality is that the labor market is very tight, industrial space is tight, and these factors all play into the importance of automation, the value it can bring, and the speed of the payback. We are in active times right now as we move deeper into the realm of e-commerce, so it's not surprising to see responses like healthy capex plans, more automation, and more people realizing they need good data with which to make smart decisions.”

“The need to automate more aspects of an operation and find further efficiencies is certainly on the forefront for managers,” says Saenz. “The reality is that the labor market is very tight, industrial space is tight, and these factors all play into the importance of automation, the value it can bring, and the speed of the payback. We are in active times right now as we move deeper into the realm of e-commerce, so it's not surprising to see responses like healthy capex plans, more automation, and more people realizing they need good data with which to make smart decisions.”

Most participating companies in 2019 came from manufacturing (41%), followed by distributors (24%), third-party logistics providers (15%), and retailers (6%). Leading verticals included food and grocery; building, construction & HVAC materials; automotive and aviation; electronics; and pharmaceuticals and health care products. Average revenue size of respondent companies dipped compared to last year's survey.

Operations profile

The impact of e-commerce can be seen in the breakdown of outbound and inbound operations among those surveyed. This year, on the outbound side, 3% had split case only, down 2% from last year, but 22% said that the nature of outbound was case and split case, up from 13% last year. That means a quarter of respondents are shipping case and split case (or split case only), up from 18% last year. Full pallet outbound only remained at 10%.

On the inbound side, full pallet only on the inbound rose from 10% last year to 19% this year. This may just be a fluctuation in the response base, but it also may be related to the impact of tariffs and global trade uncertainty, notes Saenz, with perhaps more operations importing in greater bulk this year.

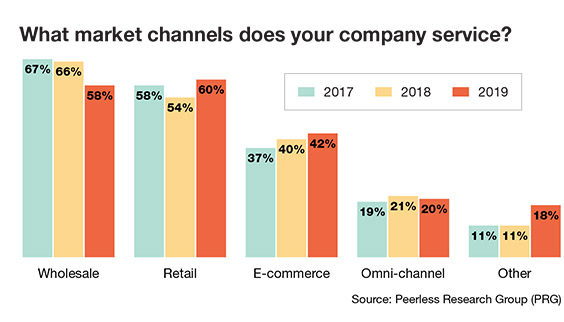

While in recent years wholesale was the most common channel serviced, a 6% jump in those servicing retailers made retail the top channel serviced (60%), followed closely by wholesale at 58%. The growth of e-commerce can also be seen by the fact that 42% now service e-commerce, up from 40% last year, while 20% say they are omni-channel, down 1% from last year. That means more than 60% either say they service e-commerce or omni-channel.

How multiple channels are being fulfilled saw a decrease in those saying they self-distribute from one DC, which deceased from 39% last year, to 36% this year. Self-distributing from separate DCs also decreased, from 24% in 2018, to 20% this year. Meanwhile, those using third party logistics (3PL) partners for all channels was up by 1%, as was those using 3PLs for e-commerce only, while using their own DCs for other channels.

How multiple channels are being fulfilled saw a decrease in those saying they self-distribute from one DC, which deceased from 39% last year, to 36% this year. Self-distributing from separate DCs also decreased, from 24% in 2018, to 20% this year. Meanwhile, those using third party logistics (3PL) partners for all channels was up by 1%, as was those using 3PLs for e-commerce only, while using their own DCs for other channels.

Interestingly, the geographic scope of DC networks also shifted. Those saying they cover the entire U.S. market with their operations declined from 32% last year, to 24% this year. Conversely, there were increases in those focused on a single metro area, or multi-state region. According to Derewecki, such responses could reflect the beginnings of a trend among DC operators of trying to position DCs closer to customers in densely populated areas to facilitate same-day fulfillment.

“When companies are promising consumers very rapid deliveries, the only way to really support that, after you maximize your internal response time within the DC, is to get closer to customers,” says Derewecki. “While there may just be some year-to-year variation in the survey, it will be interesting to see if future year results on questions like geographic scope point to a real trend of putting more facilities closer to customers to support the type of hyper-local fulfillment concepts that are emerging. Right now, it's hard to make that conclusion, but it will be interesting to watch.”

There were some surprises with key operational elements. For example, the number of respondents with more than three building in the DC network declined from 41% last year, to 36% this year. However, of those with three-plus buildings, 26% have more than six facilities, down just 1% from last year.

Another surprising result, given that e-commerce often involves a larger assortment of stock keeping units (SKUs), is that average number of SKUs dropped from 13,985 last year, to 10,615 this year. Inventory turns also declined slightly, from 8.9 annual turns last year, to 8.2 turns this year.

However, when asked about areas of expansion for the coming 12 months, 24% will try to increase turns, up from 17% last year, and 39% plan on more SKUs, up from 33% last year.

Average annual revenue size for respondents did fall from $1.25 billion to just over $1 billion this, so to some extent, this could cause variation on answers for questions like SKUs counts or size of DC network.

Going forward, more respondents do anticipate larger SKU counts and the need to increase turns. “From what we see with our clients, there is a trend to larger SKU counts related to the inventory assortment typically needed to service e-commerce, but at the same time, the other trend is that people are looking to get rid of old SKUs,” says Saenz. “Cleaning up obsolete SKUs is an area which needs more attention.”

Space and labor trends

This year's survey results saw a break from the trend toward bigger, taller DCs the last few years. For example, average square footage for a facility dropped from 220,800 sq. ft. last year to 183,750 this year. However, among respondents whose networks have four or more buildings, average square footage continued to climb, up from 279,825 sq. ft. last year to 285,000 this year. Given that these are likely larger companies with extensive DC networks, it's possible the trend is to be constructing new, larger DCs rather than leasing existing space that might involve smaller buildings.

This year's survey results saw a break from the trend toward bigger, taller DCs the last few years. For example, average square footage for a facility dropped from 220,800 sq. ft. last year to 183,750 this year. However, among respondents whose networks have four or more buildings, average square footage continued to climb, up from 279,825 sq. ft. last year to 285,000 this year. Given that these are likely larger companies with extensive DC networks, it's possible the trend is to be constructing new, larger DCs rather than leasing existing space that might involve smaller buildings.

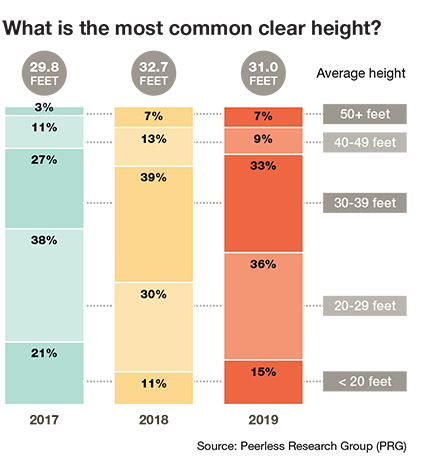

Similarly, clear heights were down slightly. This year, average clear height was 31 feet, down from 32.7 ft. last year, but taller than in 2017. According to Saenz, a possible reason for this finding is that some respondents may lease smaller existing space with lower clear heights, while those doing new construction are building facilities at least 32 ft. high or higher.

When it comes to expansion plans, 79% are planning some type of expansion, which shows optimism around expected volumes. Those planning to expand the number of SKUs grew by 6% compared to 2018, and 24% plan to increase turns, up from 17% last year.

However, those planning to increase the number of employees decreased a bit to 30% this year from 33% last year, while expected increase in total square footage fell from 29% last year to 26% this year. These relatively modest differences may reflect a variation in response pool, or a trend toward using more automation at slightly smaller DCs.

With space utilization during peak season, average peak utilization came in at 82.5% this year, compared to 86.3% last year. Many had higher peak utilization, with 39% reporting peak utilization of 85% to 94%, and 20% having peak utilization of 95% or more.

The most congested DC area was the shipping dock, with 31% naming it as the most congested area, compared to 22% last year. It is fairly commonplace, explains Saenz, for dock areas to become congested, especially with the shift toward more frequent less-than truckload (LTL) and parcel carrier pickups, and adaptation to DC layouts over time.

“The dock area is typically where you'll see bottlenecks, in part because of layout design factors. Sometimes, the dock area is unfortunately undersized from the start, or if it's sized properly, the space ends up shrinking over time because of changes like adding more racks to the end of aisles. Dock area congestion is a key indicator of a well-planned and operated facility, and is critical to the throughput of a facility.”

“The dock area is typically where you'll see bottlenecks, in part because of layout design factors. Sometimes, the dock area is unfortunately undersized from the start, or if it's sized properly, the space ends up shrinking over time because of changes like adding more racks to the end of aisles. Dock area congestion is a key indicator of a well-planned and operated facility, and is critical to the throughput of a facility.”

Projected annual capex for warehousing systems and equipment in 2020 reached an average of $1.27 million, just a hair over last year's average of $1.26. The median shrank due to some smaller company respondents, but still, 27% of respondents will spend in upwards of $1 million next year. That's 1% higher than last year.

For 2019, the average number of employees in the main warehouse was at 175 employees, down a bit from last year's 182 employees. This could be a function of this year's respondent pool, but also might reflect the use of more automation.

Interestingly, the percentage of the workforce that is “temporary” during peak season declined a bit. Last year, 19.1% were temps, while this year, that figure declined to 14.1%. Given unemployment rates that are at or near historic lows this past year, and the difficulties in training temporary workers on proper warehouse procedures, it may be that slightly more companies are looking to automate some tasks, or looking to recruit more full-time workers.

Interestingly, the percentage of the workforce that is “temporary” during peak season declined a bit. Last year, 19.1% were temps, while this year, that figure declined to 14.1%. Given unemployment rates that are at or near historic lows this past year, and the difficulties in training temporary workers on proper warehouse procedures, it may be that slightly more companies are looking to automate some tasks, or looking to recruit more full-time workers.

“Finding enough qualified labor has become so hard that it may well be that more companies are realizing that they can't rely on such a high mix of temps in their labor force,” explains Derewecki. “By the time you have them trained up to be really effective, the peak might be gone.”

This year the survey introduced some questions about pay increases and how to cope with rising pay rates. The survey showed action being taken by respondents to solidify their workforces, with 54% saying they've increased pay and 38% telling us that they're improving benefits. Only 25% said they haven't increased pay.

What's more, 68% are enhancing processes or training to improve productivity, while 68% affirmed that they're developing training or employee retention programs. At the same time, 38% said they're increasing use of automation, mechanization, or other labor-saving technologies.

Given that few operations can completely automate, what's likely happening, explains Derewecki, is a two-fold strategy of trying to attract and retain a reliable pool of workers and automate selectively. “For many operators in metro areas, it's a very competitive landscape to try to find labor today,” says Derewecki. “As a result, we really do see more companies making an effort at workforce development, not only with pay, but in areas like training. There generally is more of the attitude that, ‘yes, our people are a key asset.'”

Tech and automation

As noted, one approach to mitigating the risk of not being able to find enough labor is to use more automation. Other findings in the survey also reflect the use of more automation, although some tech findings—such as warehouse management system (WMS) use—declined a bit versus 2018.

For example, with materials handling systems, manual approaches are still widely used. Manual picking was used by 72%, a decline from 76% last year. On the other hand, use of automated replenishment was up by 7%, and use of automated storage & retrieval (ASRS) solutions climbed from 12% last year to 15% this year. Also on the rise was use of robotic/articulating arms, which increased from 3% to 4%.

When asked about specific picking technologies, paper-based approaches did see a 7% increase versus last year, but parts-to-person automation doubled from 7% last year to 14% this year. Voice assisted solution approaches also climbed from 12% last year to 14% this year.

Use of WMS came in at 85%, a decrease from last year's 93%, but very close to the WMS usage levels for 2017 and 2016. As was the case the year before, the two most popular WMS approaches are warehouse management as an enterprise resource planning (ERP) system module, or a legacy/homegrown system. Use of best-of-breed WMS stayed fairly steady at 18%, 1% less than last year. Also staying steady was the 6% who leverage a warehouse execution system (WES).

Perhaps more surprising was that 58% said they were using manual data collection this year, up from 53% last year. While the change isn't large, there are circumstances that might explain some more manual methods, such as companies needing to ramp up sites quickly, more startups as respondents, or more use of 3PLs.

On balance, there were plenty of findings that affirm rising technology use. For example, 23% said “adding automation equipment to processes” was a key action taken to lower costs, up from 15% last year, while 45% said improving warehouse information technology (IT) was a key action to manage costs. The same cost management question showed that use of 3PLs rose a bit, from 15% last year to 18% this year.

This year's respondents showed interest in data quality issues that impact the proper use of warehouse automation and related software. In particular, 23% say that lack of adequate SKU weight and dimension (DIM) data is a major issue, an increase from 16% last year. In a separate question, only 40% of respondents said they have complete SKU weights and DIMs in their item masters.

While such data issues might seem to be a minor IT housekeeping concern, accurate weights and DIMs are essential to the functioning of proper slotting and warehouse automation such as sorters, shuttles, and ASRSs, in addition being needed by many WMS solutions, notes Derewecki. “The survey results showed some good movement in regards to the importance of getting this data,” he says. “The more automated a facility is, the more important this data is.”

Saenz agrees on the importance of data to fully reap the benefits of technology. “As more and more people start opening their eyes to advanced automation and the use of advanced WMS functionality, they're going to realize that they must have the fundamental data elements in place, and keep it updated, so their systems work the way they expect them to work,” he says.

Saenz agrees on the importance of data to fully reap the benefits of technology. “As more and more people start opening their eyes to advanced automation and the use of advanced WMS functionality, they're going to realize that they must have the fundamental data elements in place, and keep it updated, so their systems work the way they expect them to work,” he says.

Many factors must come together for DCs to function well in this current climate, says Saenz. Having enough capex, applying more technology, figuring out how to attract enough labor, are all part of the mix, he concludes. “DC operations face many challenges and changes, and e-commerce is just pushing the need for change that much faster,” he says. “But it's apparent that managers see the value of automation, and not just the technology itself, but the need for good data and processes to get the most from their investments.”

SC

MR

Sorry, but your login has failed. Please recheck your login information and resubmit. If your subscription has expired, renew here.

November 2019

We hear a lot about emerging technologies like artificial intelligence, machine learning and robotics. We hear less about one of the enabling technologies that makes the others possible: Browse this issue archive. Access your online digital edition. Download a PDF file of the November 2019 issue.In last year's “Warehouse and Distribution Center (DC) Operations Survey,” the tight labor market stood out as the overriding challenge for warehouse operations managers. For the 2019 edition, not only did labor scarcity remain the top challenge, but also the results show that respondents are taking action to mitigate the problem.

In fact, this year's respondents report that they're using multiple methods of strengthening their workforces. One of these is increasing pay, which 54% said that they did this year. Other strategies include enhanced training and better benefits.

These struggles to find and retain an effective workforce are being done against a backdrop of continued business growth and the ongoing impact of e-commerce fulfillment activity. For 2019, 42% are involved in e-commerce, and 20% said that they service an omni-channel environment. Other telling data points are outlined below.

- Business confidence appears solid: When asked if their operation was planning to expand in the next 12 months, 79% said, “yes,” which is 3% higher than last year.

- Capital expenditure (capex) plans remained healthy. The average projected capex for the next year was $1.27 million, nearly identical to last year. While the average respondent was at a smaller operation this year, which likely lowered the median, 9% plan to spend $10 million or more.

- Inability to attract and retain a qualified hourly workforce was again the leading industry issue, cited by 50% of respondents. This was down a bit from last year, but those concerned about the inability to find good supervisors shot up from 26% last year to 35% this year.

- Responses around technology use were mixed in some regards, but generally pointed toward a continued surge in the willingness to apply automation and software. For example, on a question about actions for managing DC costs, 23% said they were adding automation to contain costs, up from 15% last year.

The survey, conducted annually by Peerless Research Group, drew 146 responses this year from professionals in logistics and warehouse operations across multiple verticals. According to Norm Saenz, Jr., a managing director with St. Onge Company, and Don Derewecki, a senior consultant with St. Onge Company, a supply chain engineering consulting company and our partner for this annual survey, respondents are coping with many areas of change, with a common strategy being the use of more technology.

“The pace of change is increasing every year, which needs to be accounted for,” says Derewecki. “This year's survey shows respondents are budgeting for change; they're looking to use more technology and automation; and they are looking to improve their operational processes and controls.”

Saenz agrees that managers responsible for DC operations are focused on ways to find efficiencies to help cope with the impacts of e-commerce growth, and to help mitigate labor scarcity.

“The need to automate more aspects of an operation and find further efficiencies is certainly on the forefront for managers,” says Saenz. “The reality is that the labor market is very tight, industrial space is tight, and these factors all play into the importance of automation, the value it can bring, and the speed of the payback. We are in active times right now as we move deeper into the realm of e-commerce, so it's not surprising to see responses like healthy capex plans, more automation, and more people realizing they need good data with which to make smart decisions.”

Most participating companies in 2019 came from manufacturing (41%), followed by distributors (24%), third-party logistics providers (15%), and retailers (6%). Leading verticals included food and grocery; building, construction & HVAC materials; automotive and aviation; electronics; and pharmaceuticals and health care products. Average revenue size of respondent companies dipped compared to last year's survey.

Operations profile

The impact of e-commerce can be seen in the breakdown of outbound and inbound operations among those surveyed. This year, on the outbound side, 3% had split case only, down 2% from last year, but 22% said that the nature of outbound was case and split case, up from 13% last year. That means a quarter of respondents are shipping case and split case (or split case only), up from 18% last year. Full pallet outbound only remained at 10%.

On the inbound side, full pallet only on the inbound rose from 10% last year to 19% this year. This may just be a fluctuation in the response base, but it also may be related to the impact of tariffs and global trade uncertainty, notes Saenz, with perhaps more operations importing in greater bulk this year.

While in recent years wholesale was the most common channel serviced, a 6% jump in those servicing retailers made retail the top channel serviced (60%), followed closely by wholesale at 58%. The growth of e-commerce can also be seen by the fact that 42% now service e-commerce, up from 40% last year, while 20% say they are omni-channel, down 1% from last year. That means more than 60% either say they service e-commerce or omni-channel.

How multiple channels are being fulfilled saw a decrease in those saying they self-distribute from one DC, which deceased from 39% last year, to 36% this year. Self-distributing from separate DCs also decreased, from 24% in 2018, to 20% this year. Meanwhile, those using third party logistics (3PL) partners for all channels was up by 1%, as was those using 3PLs for e-commerce only, while using their own DCs for other channels.

Interestingly, the geographic scope of DC networks also shifted. Those saying they cover the entire U.S. market with their operations declined from 32% last year, to 24% this year. Conversely, there were increases in those focused on a single metro area, or multi-state region. According to Derewecki, such responses could reflect the beginnings of a trend among DC operators of trying to position DCs closer to customers in densely populated areas to facilitate same-day fulfillment.

“When companies are promising consumers very rapid deliveries, the only way to really support that, after you maximize your internal response time within the DC, is to get closer to customers,” says Derewecki. “While there may just be some year-to-year variation in the survey, it will be interesting to see if future year results on questions like geographic scope point to a real trend of putting more facilities closer to customers to support the type of hyper-local fulfillment concepts that are emerging. Right now, it's hard to make that conclusion, but it will be interesting to watch.”

There were some surprises with key operational elements. For example, the number of respondents with more than three building in the DC network declined from 41% last year, to 36% this year. However, of those with three-plus buildings, 26% have more than six facilities, down just 1% from last year.

Another surprising result, given that e-commerce often involves a larger assortment of stock keeping units (SKUs), is that average number of SKUs dropped from 13,985 last year, to 10,615 this year. Inventory turns also declined slightly, from 8.9 annual turns last year, to 8.2 turns this year.

However, when asked about areas of expansion for the coming 12 months, 24% will try to increase turns, up from 17% last year, and 39% plan on more SKUs, up from 33% last year.

Average annual revenue size for respondents did fall from $1.25 billion to just over $1 billion this, so to some extent, this could cause variation on answers for questions like SKUs counts or size of DC network.

Going forward, more respondents do anticipate larger SKU counts and the need to increase turns. “From what we see with our clients, there is a trend to larger SKU counts related to the inventory assortment typically needed to service e-commerce, but at the same time, the other trend is that people are looking to get rid of old SKUs,” says Saenz. “Cleaning up obsolete SKUs is an area which needs more attention.”

Space and labor trends

This year's survey results saw a break from the trend toward bigger, taller DCs the last few years. For example, average square footage for a facility dropped from 220,800 sq. ft. last year to 183,750 this year. However, among respondents whose networks have four or more buildings, average square footage continued to climb, up from 279,825 sq. ft. last year to 285,000 this year. Given that these are likely larger companies with extensive DC networks, it's possible the trend is to be constructing new, larger DCs rather than leasing existing space that might involve smaller buildings.

Similarly, clear heights were down slightly. This year, average clear height was 31 feet, down from 32.7 ft. last year, but taller than in 2017. According to Saenz, a possible reason for this finding is that some respondents may lease smaller existing space with lower clear heights, while those doing new construction are building facilities at least 32 ft. high or higher.

When it comes to expansion plans, 79% are planning some type of expansion, which shows optimism around expected volumes. Those planning to expand the number of SKUs grew by 6% compared to 2018, and 24% plan to increase turns, up from 17% last year.

However, those planning to increase the number of employees decreased a bit to 30% this year from 33% last year, while expected increase in total square footage fell from 29% last year to 26% this year. These relatively modest differences may reflect a variation in response pool, or a trend toward using more automation at slightly smaller DCs.

With space utilization during peak season, average peak utilization came in at 82.5% this year, compared to 86.3% last year. Many had higher peak utilization, with 39% reporting peak utilization of 85% to 94%, and 20% having peak utilization of 95% or more.

The most congested DC area was the shipping dock, with 31% naming it as the most congested area, compared to 22% last year. It is fairly commonplace, explains Saenz, for dock areas to become congested, especially with the shift toward more frequent less-than truckload (LTL) and parcel carrier pickups, and adaptation to DC layouts over time.

“The dock area is typically where you'll see bottlenecks, in part because of layout design factors. Sometimes, the dock area is unfortunately undersized from the start, or if it's sized properly, the space ends up shrinking over time because of changes like adding more racks to the end of aisles. Dock area congestion is a key indicator of a well-planned and operated facility, and is critical to the throughput of a facility.”

Projected annual capex for warehousing systems and equipment in 2020 reached an average of $1.27 million, just a hair over last year's average of $1.26. The median shrank due to some smaller company respondents, but still, 27% of respondents will spend in upwards of $1 million next year. That's 1% higher than last year.

For 2019, the average number of employees in the main warehouse was at 175 employees, down a bit from last year's 182 employees. This could be a function of this year's respondent pool, but also might reflect the use of more automation.

Interestingly, the percentage of the workforce that is “temporary” during peak season declined a bit. Last year, 19.1% were temps, while this year, that figure declined to 14.1%. Given unemployment rates that are at or near historic lows this past year, and the difficulties in training temporary workers on proper warehouse procedures, it may be that slightly more companies are looking to automate some tasks, or looking to recruit more full-time workers.

“Finding enough qualified labor has become so hard that it may well be that more companies are realizing that they can't rely on such a high mix of temps in their labor force,” explains Derewecki. “By the time you have them trained up to be really effective, the peak might be gone.”

This year the survey introduced some questions about pay increases and how to cope with rising pay rates. The survey showed action being taken by respondents to solidify their workforces, with 54% saying they've increased pay and 38% telling us that they're improving benefits. Only 25% said they haven't increased pay.

What's more, 68% are enhancing processes or training to improve productivity, while 68% affirmed that they're developing training or employee retention programs. At the same time, 38% said they're increasing use of automation, mechanization, or other labor-saving technologies.

Given that few operations can completely automate, what's likely happening, explains Derewecki, is a two-fold strategy of trying to attract and retain a reliable pool of workers and automate selectively. “For many operators in metro areas, it's a very competitive landscape to try to find labor today,” says Derewecki. “As a result, we really do see more companies making an effort at workforce development, not only with pay, but in areas like training. There generally is more of the attitude that, ‘yes, our people are a key asset.'”

Tech and automation

As noted, one approach to mitigating the risk of not being able to find enough labor is to use more automation. Other findings in the survey also reflect the use of more automation, although some tech findings—such as warehouse management system (WMS) use—declined a bit versus 2018.

For example, with materials handling systems, manual approaches are still widely used. Manual picking was used by 72%, a decline from 76% last year. On the other hand, use of automated replenishment was up by 7%, and use of automated storage & retrieval (ASRS) solutions climbed from 12% last year to 15% this year. Also on the rise was use of robotic/articulating arms, which increased from 3% to 4%.

When asked about specific picking technologies, paper-based approaches did see a 7% increase versus last year, but parts-to-person automation doubled from 7% last year to 14% this year. Voice assisted solution approaches also climbed from 12% last year to 14% this year.

Use of WMS came in at 85%, a decrease from last year's 93%, but very close to the WMS usage levels for 2017 and 2016. As was the case the year before, the two most popular WMS approaches are warehouse management as an enterprise resource planning (ERP) system module, or a legacy/homegrown system. Use of best-of-breed WMS stayed fairly steady at 18%, 1% less than last year. Also staying steady was the 6% who leverage a warehouse execution system (WES).

Perhaps more surprising was that 58% said they were using manual data collection this year, up from 53% last year. While the change isn't large, there are circumstances that might explain some more manual methods, such as companies needing to ramp up sites quickly, more startups as respondents, or more use of 3PLs.

On balance, there were plenty of findings that affirm rising technology use. For example, 23% said “adding automation equipment to processes” was a key action taken to lower costs, up from 15% last year, while 45% said improving warehouse information technology (IT) was a key action to manage costs. The same cost management question showed that use of 3PLs rose a bit, from 15% last year to 18% this year.

This year's respondents showed interest in data quality issues that impact the proper use of warehouse automation and related software. In particular, 23% say that lack of adequate SKU weight and dimension (DIM) data is a major issue, an increase from 16% last year. In a separate question, only 40% of respondents said they have complete SKU weights and DIMs in their item masters.

While such data issues might seem to be a minor IT housekeeping concern, accurate weights and DIMs are essential to the functioning of proper slotting and warehouse automation such as sorters, shuttles, and ASRSs, in addition being needed by many WMS solutions, notes Derewecki. “The survey results showed some good movement in regards to the importance of getting this data,” he says. “The more automated a facility is, the more important this data is.”

Saenz agrees on the importance of data to fully reap the benefits of technology. “As more and more people start opening their eyes to advanced automation and the use of advanced WMS functionality, they're going to realize that they must have the fundamental data elements in place, and keep it updated, so their systems work the way they expect them to work,” he says.

Many factors must come together for DCs to function well in this current climate, says Saenz. Having enough capex, applying more technology, figuring out how to attract enough labor, are all part of the mix, he concludes. “DC operations face many challenges and changes, and e-commerce is just pushing the need for change that much faster,” he says. “But it's apparent that managers see the value of automation, and not just the technology itself, but the need for good data and processes to get the most from their investments.”

SC

MR

More WMS

- Innovators Netstock, Pickle Robot win NextGen Solution Provider awards

- NextGen Supply Chain Conference unveils agenda focused on AI, execution and the future of leadership

- Wayfair executive to share lessons from building a tech-driven delivery network in NextGen Keynote

- Eli Lilly’s Mar Gimeno to keynote at NextGen Supply Chain Conference 2026

- Your 3PL has EDI, and then what?

- NextGen extends 2026 award, speaker submission deadlines amid strong industry interest

- More WMS

Latest Podcast

Explore

Explore

Topics

Business Management News

- Innovators Netstock, Pickle Robot win NextGen Solution Provider awards

- Bigger trucks versus broken bridges and roads

- From salon to dock door: Repurposing scheduling software for inbound flow

- The biggest barrier to AI in supply chains isn’t technology

- Rebuilding a planning function around the physical world

- Why companies blame the wrong supplier … and miss the real failure

- More Business Management

Latest Business Management Resources

About the Author

Roberto Michel, Editor at Large

Roberto Michel, senior editor for Modern, has covered manufacturing and supply chain management trends since 1996, mainly as a former staff editor and former contributor at Manufacturing Business Technology. He has been a contributor to Modern since 2004. He has worked on numerous show dailies, including at ProMat, the North American Material Handling Logistics show, and National Manufacturing Week. You can reach him at: [email protected].

Follow SCMR on social media.

@SupplyChainManagementReview on Facebook

@SCMR on Twitter

SCMR on Linkedin

Subscribe

Supply Chain Management Review delivers the best industry content.

Editors’ Picks