For more than 40 years, companies operating in Europe have been designing their supply chains for a trade regime of minimal paperwork and zero tariffs. Brexit could turn this low cost, low friction system on its head—or maybe it won't. Uncertainty about the final outcome, how long negotiations will take and a possible transition period creates a huge dilemma for leadership teams.

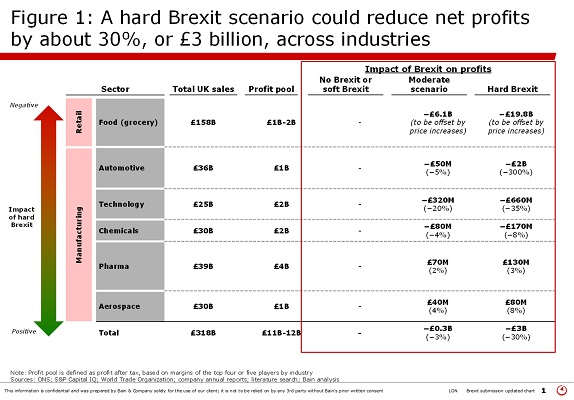

A hard Brexit poses substantial risk to the profitability of companies operating in the UK. Disruptions to supply chains, for example, could reduce net profits of five key manufacturing industries alone by as much as 30%, or £3 billion, with automotive and technology industries among the hardest hit, according to analysis by Bain & Company (see Figure 1).

Figure 1

But preparing now for a hard Brexit scenario may backfire on companies. It's likely to take two years or longer for the UK to agree on the terms of the UK's future relationship with the EU, once the UK government invokes Article 50 of the Lisbon Treaty. If the UK ends up with more favorable terms, companies that move manufacturing or sourcing out of the UK risk incurring a higher cost base unnecessarily.

That double peril has left many leadership teams anxious and reluctant to act. But waiting for a clearer sense of the future is the riskiest option. Companies can limit the negative consequences of Brexit by studying the range of future scenarios and developing a strategy that anticipates change.

Management teams that have learned to manage in uncertainty focus on the few risks that matter most. They assess each potential scenarios and identify the critical trigger points that signal a swing from one outcome to another—we call these signposts. That approach helps determine a clear portfolio of strategic actions that balance commitment and flexibility. Instead of basing a strategy on a discrete outcome, companies bracing for change engage in a continuous cycle of execute, monitor and adapt, redirecting the company toward the best opportunities over time.

Potential Brexit fallout

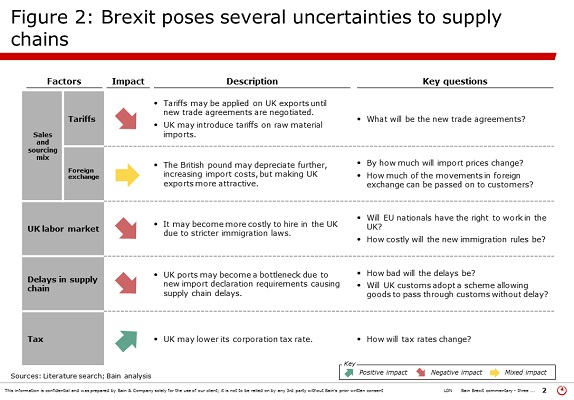

Future Brexit scenarios range from no change at all to severe change. While that may feel overwhelming, a handful of factors will determine how significantly Brexit will disrupt companies' supply chains: tariffs, foreign exchange rates and the UK's labor market regulations, immigration laws and tax policy (see Figure 2).

Figure 2

A hard Brexit could include a shift to standard WTO tariffs (2% to 13%) on all exports and imports, a 10% increase in the cost of UK labor and a 20% depreciation in the British pound. A moderate scenario could involve a rise of up to 5% in export and import tariffs, a 10% currency depreciation and a 5% increase in the cost of labor. Ultimately, the UK might still land on a softer Brexit, with minimal or no tariffs on trade with the EU. The Prime Minister has made a commitment to put the final deal to a vote in both Houses of Parliament, which seems appropriate for the oldest surviving representative democracy, but this itself adds uncertainty.

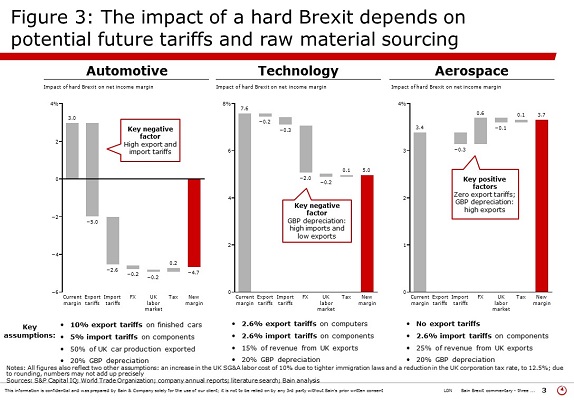

A hard Brexit poses the biggest risk for the food retail, automotive and technology industries. These three sectors would see the greatest negative impact on profits from import and export tariffs, higher inventory requirements to compensate for procurement bottlenecks and delays, and a depreciation of the British pound. Food retailers could see profits fall by £6 billion to £20 billion, though most would seek to offset part of that decline with price increases. Technology companies could suffer a 20% to 35% decline in profit while chemical companies may see a drop of 4% to 8% (see Figures 1 and 3), depending on their ability to pass on some price increases.

Figure3

On the other hand, net exporters in industries with low WTO tariffs, such as aerospace, or industries characterized by zero tariffs and a global production footprint and sales mix, such as pharma, could potentially benefit from a hard Brexit due to pound depreciation and lower UK tax rates. In this scenario, aerospace companies may see profits increase by 4% to 8%, and pharma, by 2% to 3%. Indeed, large industrial and pharma companies, including Rolls-Royce, Boeing, GSK and AstraZeneca, have confirmed their commitment to continue investing in the UK.

Importantly, Brexit's impact may vary even within a given industry, because each company's supply chain is different. Associated British Foods, which produces more than two million tonnes of sugar annually from sugar beet factories in the UK and Spain, could be hit hard if Brexit triggers a shift to WTO customs duties on sugar beet. By contrast, Tate & Lyle Sugars, one of Europe's largest sugar manufacturers, currently pays high EU tariffs on sugar cane imports from Brazil. If the UK agrees after Brexit to the more favorable WTO tariff structure on non-EU sugar cane imports, Tate & Lyle Sugars could import and produce at lower cost.

A strategy for Brexit uncertainty

Companies that develop a strategy for uncertainty will be able to pivot faster than the competition when Brexit details become clear, minimizing supply chain risk. Four guidelines can help leadership teams understand how Brexit could play out for them:

define the specific uncertainties your business might face and their economic impact on your company (absolute and relative);

formulate a set of probable scenarios and their economic impact;

devise a specific set of strategic options; and

- identify a clear set of signposts for action.

Leading companies use that approach to balance commitment to a long-term supply chain strategy with investments and to position themselves to seize the post-Brexit future as it unfolds. Timing is key, no matter which scenario unfolds. While planning rational actions for each possible outcome, leaders pair each action with a signpost that triggers it.

No-regret moves. Some actions will increase a company's competitive edge no matter what scenario plays out. They include improving cost management or operational effectiveness. One UK retailer decided it would be better off setting up a global warehouse hub outside the UK to position itself both for the possibility of a medium or hard Brexit and for geographical advantage.

Options and hedges. Leadership teams that develop strategic options and hedges for a variety of future scenarios navigate better when new developments unfold. Lloyd's of London, which generates 11% of its revenues from Europe, announced it will move part of its operations to the EU in 2017 since Brexit is likely to eliminate the passporting rights that allow EU companies to sell their services across borders.

Companies manufacturing in the UK can hedge against a hard Brexit by investing in a range of smaller-scale pilot plants in the EU that can be ramped up or scaled down quickly. Producing small volumes allows companies to keep costs down while learning about manufacturing in a new country. If the UK opts for a hard Brexit, companies with pilot plants outside the UK are well positioned to quickly relocate or ramp up production. In the case of a soft Brexit, the company has avoided a large and ultimately unnecessary investment.

Other options include joint ventures that provide lower cost market entry or manufacturing changes that provide additional flexibility at low cost. Some companies exposed to a devaluation of the pound may use financial hedging instruments or choose to denominate contracts in different currencies.

Big bets. The most challenging balancing act involves large-scale investments that have different payoffs depending how future uncertainties play out. Examples include doubling down on UK production capacity, shifting production to new foreign markets and switching suppliers from foreign- to UK-based companies.

Automaker Nissan's decision to manufacture new models in the UK is a big bet that the UK will negotiate a zero-for-zero arrangement with the EU, meaning neither will impose tariffs on finished cars and components. Toyota, by contrast, is waiting for a clearer signal on the future of UK-EU tariff regime for autos. The EU currently imposes a 10% tariff on finished cars entering the common market. Roughly 50% of cars manufactured in the UK are exported, and 65% of car components are sourced from outside the UK.

Leading companies develop flexibility by focusing on projects that make sense now while assessing their payoffs under different future scenarios. If a big bet looks too risky to take immediately, companies can wait for greater clarity and move quickly once signposts—such as the final UK-EU agreement, other foreign trade agreements and budget announcements—signal likely changes ahead.

It will take two years to know what changes Brexit will bring and how they will affect supply chain speed, costs and inventories. Company leaders that anticipate multiple outcomes will have the best odds of navigating this period of uncertainty successfully. Developing a strategy for uncertainty provides leadership teams with the tools to anticipate multiple Brexit outcomes ahead of the competition—and long before the government makes its final decision.

By incorporating change into the strategic process, companies can pivot and correct course quickly as Brexit unfolds. That kind of agility may also help companies brace for other future supply chain risks, from the possible instability or breakup of the eurozone to changing US trade policy under the Trump administration.

Michael Garstka and Thomas Kwasniok are partners in Bain & Company's London office. Pete Guarraia is a partner in Bain's Chicago office.

SC

MR

Latest Supply Chain News

- The biggest barrier to AI in supply chains isn’t technology

- Rebuilding a planning function around the physical world

- Why companies blame the wrong supplier … and miss the real failure

- NextGen Supply Chain Conference unveils agenda focused on AI, execution and the future of leadership

- From fragmented negotiations to coordinated negotiation performance: an AI-enabled approach

- More News

Latest Resources

Explore

Explore

Latest Supply Chain News

- Why companies blame the wrong supplier … and miss the real failure

- NextGen Supply Chain Conference unveils agenda focused on AI, execution and the future of leadership

- From fragmented negotiations to coordinated negotiation performance: an AI-enabled approach

- Supply chain resilience isn’t a data problem; it’s a judgment problem

- Beyond the hype: Building flexible and scalable supply chains in a VUCA world

- Why your supply chain risk management plan will fail

- More latest news

Latest Resources

Subscribe

Supply Chain Management Review delivers the best industry content.

Editors’ Picks