Logistics and transportation is an intricate puzzle of interconnected routes, carriers, shippers, modes, and supply chains. Delivering success requires these pieces to fit seamlessly together.

However, the complexity of modern operations extends beyond just the physical networks.

Today’s logistics and transportation professionals must navigate challenging market conditions and an evolving regulatory environment while competing for talent and continuously evaluating new and emerging technologies. Missing or neglecting even one piece of this puzzle can cause operational disruptions, inefficiency, and missed opportunities.

The 33rd Annual Study of Logistics and Transportation Trends explores these pieces, revealing insights into how industry leaders are working to navigate this puzzling environment and shape the path forward.

The 33rd Annual Study of Logistics and Transportation Trends surveyed more than 200 industry practitioners, 85% of whom had 15 or more years of industry experience, and 80% serve in C-level, vice president, director, or managerial roles. Participants represent organizations with fewer than 100 to more than 5,000 employees and annual revenues ranging from less than $250 million to more than $9 billion.

This year’s study examines transportation spending, competitive strategy, and performance in order to better understand how firms are executing and differentiating themselves.

Market conditions

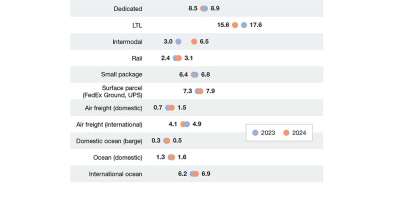

Spending. Transportation spend is a large piece of the logistics puzzle. This year, spending on private fleets dropped 50% to 7.23% of transportation spending, down from a six-year high of nearly 15%. Truckload (TL) spending has slowly increased while spending on dedicated fleets and less-than-truckload (LTL) services saw slight declines. Intermodal transport posted its highest percentage of spending over the last decade at 6.5%, while air, domestic ocean, and barge freight all increased last year.

What about the Titans, those shipper operations in companies with sales over $3 billion? These large shippers have more in common with the overall trends than they do differences. The Titans differ mainly in spending less on small package (less than 2% of spend) and LTL (under 5%). This makes intuitive sense, as larger firms are more likely to ship larger quantities, thus requiring fewer small package and LTL services.

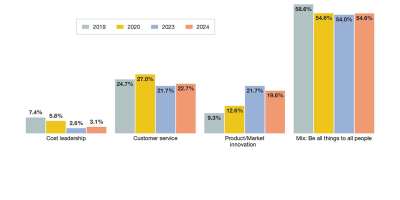

Strategy. Competitive strategy is another crucial piece of the operational environment. The most notable trend is the continued dominance of the “Mix: Be all things to all people” strategy, which remains steady at 54.6%. We believe this reflects the continued prioritization of flexibility to meet various customer needs.

In contrast, cost leadership strategies have substantially declined from 7.4% in 2019 to 3.1% in 2024, highlighting less emphasis on competing primarily through lower prices. Meanwhile, customer service remains an essential strategy for 22.7% of the companies in 2024, up from 21.7% in 2023.

More than 19% of responding shippers are now opting for a product and market innovation-focused strategy, up from just 9.3% in 2019, recognizing innovation as an increasingly important competitive differentiator.

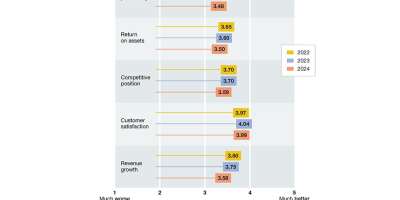

Performance. This year’s study revealed declines in all four tracked performance measures from 2023, with many of the metrics at their lowest levels in three years. When comparing their performance to competitors, shippers reported declines in firm profitability (3.48 in 2024, down from 3.74 in 2022) and return on assets (3.5 in 2024, down from 3.65 in 2022). Although customer satisfaction levels remained high (3.99 in 2024), competitive positioning (3.59 in 2024) and revenue growth (3.58 in 2024) were both down from 2023 and 2022.

Regulatory requirements

A dizzying array of government policies and regulations—which often add complexity and cost while requiring new technology and training—constitute another challenging piece of the puzzle. We included questions in this year’s study to determine the regulations that may have the most impact on operations.

Respondents were presented with various regulations and asked to indicate their impact on firm operational costs. In the survey, 64% of respondents indicate that regulations had increased operational costs by 1% to10%, while 21% say regulatory burdens increased their costs by 10% or more.

Environmental, economic/financial, and trade/customs regulations had the greatest impact on cost. Respondents believe these will continue to affect their bottom line over the next one year to three years, and they also believe that labor and employment regulations will play a

significant role. This concern is likely driven by independent contractor classification rules, such as California’s AB5, and truck driver minimum wage disputes.

Technology

Technology is another pivotal piece of the logistics and transportation puzzle. Companies must carefully consider new technologies that align with business strategy and cost-effectively deliver desired results. This year’s study provides insights into which technologies shipper organizations are adopting; drivers of their adoption decisions; and impacts of recent technology adoptions.

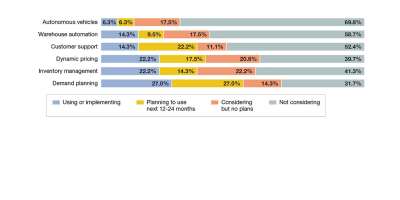

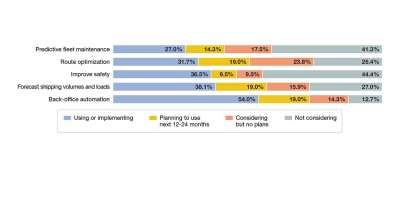

Technology adoption. The study found that 54% of respondents are using or implementing back-office automation, with another 19% planning to adopt it within 12 to 24 months. This focus on back-office automation represents a 16.2% increase in current usage from 2023.

These findings are consistent with the broader industry trend of technology investments to help streamline administrative processes and routine tasks. Participants also report the adoption of safety-related technologies (36.5% using or implementing) as well as predictive and optimization-related technologies to support improved forecasting (38.1% using or implementing) and route optimization (31.7% using or implementing).

Logistics and transportation operations seem more cautious when adopting more advanced technologies like autonomous vehicles (6.3% using or implementing) and warehouse automation (14.3% using or implementing).

Adoption drivers. Logistics and transportation operations primarily adopted technology to improve employee productivity (88.9%). Additionally, logistics operations desired technology to improve employee engagement and retention (73%).

It’s worth noting that the top two drivers are both employee-focused, reflecting intentional efforts by companies to improve employee performance and enhance the work environment. Only 39.7% of the study participants indicate that technology was adopted as part of an effort to reduce employee headcount.

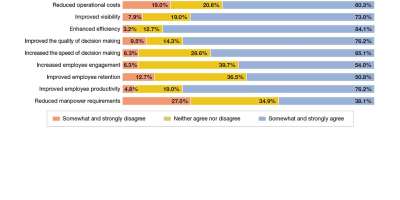

Technology benefits. It appears that most companies are achieving their employee-focused goals. More than 84% agree that recent technology adoptions have enhanced efficiency, and 76.2% reported improvements in employee productivity.

Participants also report improvements in visibility (73.0%), quality (76.2%), speed (65.1%) of decision-making, and reduced operational costs (60.3%). Participants also indicate that technology adoption makes a positive impact on employee engagement (54%) and retention (50.7%).

Talent management

The talent management piece of the logistics and transportation puzzle is incredibly complex. When this article was written (July 2024), the U.S. Chamber of Commerce reported 8.1 million job openings, but only 6.8 million unemployed workers.

This discrepancy represents a significant challenge for our labor-intensive industry. Our findings provide insights into the industry’s talent management challenges and strategies companies use to help address their requirements.

Talent gap. Participants reported challenges in finding and hiring for various positions. The most difficult-to-fill positions were those requiring experienced mid-level managers and low-wage laborers (both at 46.3%).

These results are consistent with those of other industries and governments reporting talent shortages in these areas. Sales and marketing positions (41.8%) and entry-level managers and supervisors were also difficult to fill (41.8%), further highlighting the challenges of hiring employees with leadership experience and technical skills.

Attracting talent. It is often suggested that negative perceptions of the logistics and transportation industry limit its ability to attract top talent. The Annual Study of Logistics and Transportation Trends has explored some of these perceptions over the last couple of years in hopes of identifying measures to address misperceptions and better position the industry to attract top talent.

Again, this year, participants were asked to compare logistics and transportation careers to those in other industries. Responses indicate that logistics and transportation management careers offer greater job stability as well as more opportunities for personal growth and to make meaningful organizational contributions.

These benefits can be used to promote industry career opportunities. However, logistics and transportation careers are perceived to lag other industries in flexibility, benefits, defined career paths, as well as the availability of career-related education and training. These are noteworthy areas because next-generation talent considers many of them to be critical.

Developing talent. This year’s study also the explores challenges companies face when trying to upskill and reskill employees. Results suggest many companies may have gaps between their training strategies and needs.

Participants indicate that their companies rely on in-house training programs, but only 39% of participants report that their company has a formal learning and development department.

They also indicated that the most significant challenges to upskilling and reskilling were a lack of time for training and a shortage of knowledgeable trainers within the company. This gap presents a potential risk to companies as they seek to attract new talent and help current employees develop skills needed to remain competitive.

Key takeaways

The modern logistics and transportation management puzzle has many different, complex pieces. Industry professionals navigating their path forward face challenging market conditions, an evolving regulatory environment, a rapidly changing technology landscape, and an increasingly competitive labor market.

Here are a few of our key takeaways after putting context around this year’s Annual Study of Logistics and Transportation Trends.

Invest in training and development. Whether internally or through partnerships with professional or trade associations and universities, companies should seek to offer flexible, accessible training programs that provide continuous learning opportunities tailored to individual employee needs. This investment can help companies improve employee retention and productivity while also more effectively competing for new talent.

Monitor and adapt to regulatory changes. It’s important to remain abreast of regulatory developments and proactively adapt business practices. This may seem overwhelming. While larger firms may employ or retain legal counsel to monitor regulations, others are encouraged to join industry trade groups who provide members updates on important regulatory developments. Firms who feel over-regulated should be encouraged by recent Supreme Court decisions (e.g. overturning the Chevron Doctrine) that curtail regulators’ power.

Adopting the right technology matters. According to this year’s findings, 84% of participants observed increased efficiency due to recent technology adoptions, with 76.2% also acknowledging enhancements in employee productivity. The right technology investments can also help attract new talent and address critical skill gaps.

Be a cheerleader for our industry. In this year’s study, the percentage of respondents who “strongly agree” they would recommend a career in logistics and transportation declined from 19.4% in 2022 to 18.3% in 2024. This decline underscores the importance of industry leaders and professionals being cheerleaders for our industry, actively promoting the advantages and opportunities in this field.

Adapt to market conditions. We believe the spending, strategy, and performance trends noted in this year’s study reflect the challenging conditions of the freight market. Excess capacity and changes in consumer demand have driven down rates, while operational and labor costs are increasing.

Many industry experts expect these conditions to persist for the remainder of the year and into 2025, suggesting we will continue to see performance impacts and companies adapting their spending and strategies to remain competitive and meet customer expectations.

Companies must stay agile and responsive while carefully and strategically managing their resources to navigate these challenges and sustain their performance in a volatile environment.

About the authors

Christopher A. Boone, PH.D. is an associate professor at Mississippi State Universty. Karl B. Manrodt, PH.D., is a professor at Georgia College and State University. Douglass Voss, PH.D., is a professor and the Scott E. Bennett Arkansas Highway Commission Endowed Chair at the University of Central Arkansas. Joseph Tillman is manager of education programs at SMC3.

Related presentation

SC

MR

More Transportation Management

- Transportation and logistics M&A rebounding with a focus on resilience, specialization, and tech

- 33rd Annual Study of Logistics and Transportation Trends: Unraveling the challenges ahead

- 32nd Annual Study of Logistics and Transportation Trends: Navigating a Shallow Pool of Resources

- 3PL Revenues Fall From 2021 High, But Still Grew 24% In 2022

- The latest trends in third-party logistics providers

- More Transportation Management

What's Related in Transportation Management

Explore

Explore

Topics

Business Management News

- Innovators Netstock, Pickle Robot win NextGen Solution Provider awards

- Bigger trucks versus broken bridges and roads

- From salon to dock door: Repurposing scheduling software for inbound flow

- The biggest barrier to AI in supply chains isn’t technology

- Rebuilding a planning function around the physical world

- Why companies blame the wrong supplier … and miss the real failure

- More Business Management

Latest Business Management Resources

Subscribe

Supply Chain Management Review delivers the best industry content.

Editors’ Picks