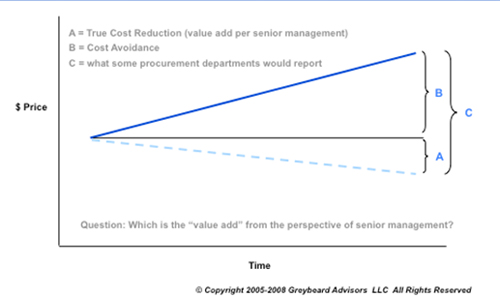

Perhaps the single most important distinction you need to make is to separate cost reduction from cost avoidance. Why do I say that? It’s simple.

Cost reduction in operating expenses can, generally, be tracked to changes in operating costs on the income statement. Cost avoidance doesn’t have the same ability. So, if you try to add cost avoidance to cost reduction, and then report your total “savings,” you’ve just created an apples & oranges amount that has absolutely no relevance to the P & L statement that your internal clients look at on a monthly basis.

That’s not to say that you should not track cost avoidance. I encourage clients to have a robust tracking system that tracks operating cost reductions, capital cost reductions, and cost avoidance. Just never add them together, or you will lose P & L relevance.

More in the next posting.

SC

MR

Latest Supply Chain News

- Procurement’s Moneyball Moment: Connecting Strategy, Sourcing, and Supply Chain Reality

- AI won’t fix a broken supply chain foundation

- How I vibe-coded an S&OP app in 30 hours

- The AI regulation gap: Risk, cost, and competitive advantage

- PepsiCo moves its startup sustainability program from pilots to operational scale across Asia Pacific

- More News

Latest Resources

Explore

Explore

Topics

Latest Supply Chain News

- PepsiCo moves its startup sustainability program from pilots to operational scale across Asia Pacific

- Eli Lilly’s Mar Gimeno to keynote at NextGen Supply Chain Conference 2026

- Agentic coding and the future of supply chain leadership

- From orbit to operations: Winning the race for the earliest disruption signal

- Stop moving boxes, start moving dollars: The new math of global supply chain velocity

- Finding your rhythm: SME supply chain footwork when the rules keep changing

- More latest news

Latest Resources

About the Author

Robert A Rudzki, SCMR Contributing Blogger

Robert A. Rudzki is a former Fortune 500 Senior Vice President & Chief Procurement Officer, who is now President of Greybeard Advisors LLC, a leading provider of advisory services for procurement transformation, strategic sourcing, and supply chain management. Bob is also the author of several leading business books including the supply management best-seller “Straight to the Bottom Line®”, its highly-endorsed sequel “Next Level Supply Management Excellence,” and the leadership book “Beat the Odds: Avoid Corporate Death & Build a Resilient Enterprise.” You can reach him through his firm’s website: www.greybeardadvisors.com

Follow SCMR on social media.

@SupplyChainManagementReview on Facebook

@SCMR on Twitter

SCMR on Linkedin

Subscribe

Supply Chain Management Review delivers the best industry content.

Editors’ Picks