Sorry, but your login has failed. Please recheck your login information and resubmit. If your subscription has expired, renew here.

May-June 2021

Indulge me for a minute, while I lead a cheer for our profession. I wrote my column for the January 2021 issue of SCMR one Sunday morning after watching the first trucks full of vaccine roll out of a Pfizer plant in Michigan, headed for a UPS sortation depot. I felt an incredible sense of optimism for the country, and pride in the role that we, as supply chain managers, were going to play to combat a pandemic. Supply chain as in the spotlight, and on that morning, it was for all the right reasons. Fast forward to late April 2021. Browse this issue archive.Need Help? Contact customer service 847-559-7581 More options

Many working in procurement view their role as saving money, either through negotiating for ever lower prices or by negotiating ever more favorable—and extended—payment terms. It’s no surprise then that one of the hottest business topics today is cash management.

This is not new. Some 20 years ago, when I led all of Bank of America’s contracting management and much of its sourcing procurement operations, we called it “float management;” a term that referred to the enterprise-wide strategic

management of cashflow in, cashflow out and overall financial benefits. My team’s projects on timing of payments out to suppliers increased annual financial benefits by significant seven figure amounts—benefits that accrued year after year. What’s not to like?

Since then, my consulting colleagues and I have advised many major companies and governmental agencies on how they too can use various payment methods and timing to increase corporate liquidity, reduce costs and receive impressive rebates. These benefits are in addition to cost savings that can be achieved through negotiation and traditional sourcing methods.

This complete article is available to subscribers only.

Log in now for full access or start your PLUS+ subscription for instant access.

SC

MR

Sorry, but your login has failed. Please recheck your login information and resubmit. If your subscription has expired, renew here.

May-June 2021

Indulge me for a minute, while I lead a cheer for our profession. I wrote my column for the January 2021 issue of SCMR one Sunday morning after watching the first trucks full of vaccine roll out of a Pfizer plant in… Browse this issue archive. Access your online digital edition. Download a PDF file of the May-June 2021 issue.Many working in procurement view their role as saving money, either through negotiating for ever lower prices or by negotiating ever more favorable—and extended—payment terms.

It’s no surprise then that one of the hottest business topics today is cash management.

This is not new. Some 20 years ago, when I led all of Bank of America’s contracting management and much of its sourcing procurement operations, we called it “float management;” a term that referred to the enterprise-wide strategic management of cashflow in, cashflow out and overall financial benefits. My team’s projects on timing of payments out to suppliers increased annual financial benefits by significant seven-figure amounts—benefits that accrued year after year. What’s not to like?

Since then, my consulting colleagues and I have advised many major companies and governmental agencies on how they too can use various payment methods and timing to increase corporate liquidity, reduce costs and receive impressive rebates. These benefits are in addition to cost savings that can be achieved through negotiation and traditional sourcing methods.

Yes, processes like strategic sourcing can initially reduce the costs of products and services bought by a company. But just re-bidding a spend segment the second or third time is not going to yield dramatically different results. After all, suppliers can only go so low and remain solvent.

Or, as Albert Einstein once said: “The definition of insanity is doing the same thing over and over again and expecting different results.”

Years ago, Strategic Procurement Solutions’ co-founder and I were invited to confer with the then-CPO of one of the largest global energy companies. I remember writing down the executive’s challenge at the time: “We have sourced everything you can possibly source, and sourcing again is not going to get us significant savings. We need to look outside of our traditional spending to find dramatic savings.” What followed was an innovative discussion of out-of-the-box ideas that leaders could deploy. Cashflow optimization was a key part of that discussion.

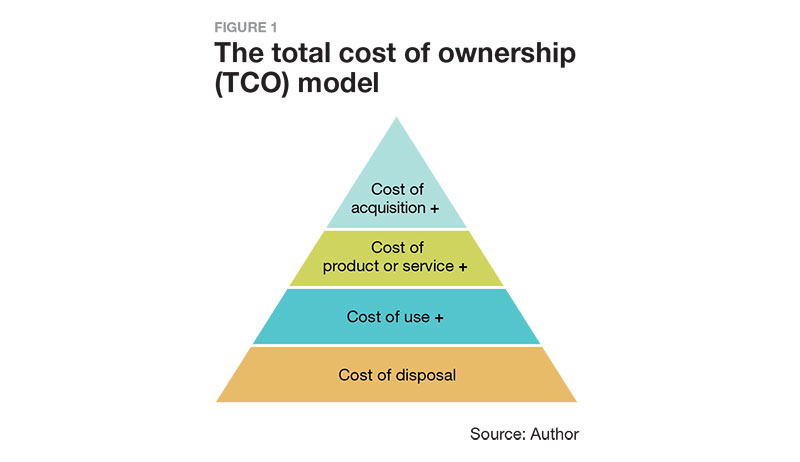

Today’s procurement methodology of category management is a major improvement over traditional sourcing because it looks more deeply at all cost elements in the total cost of ownership (TCO) model. In the training workshops that my firm conducts for procurement teams, the proper understanding of all elements of the following TCO model is one of the biggest takeaways for participants.

TCO over the lifetime of a procured product or service can be calculated using a four-pronged formula:

- cost of acquisition; plus

- cost of product or services (delivered, installed and made operative); plus

- cost of use; plus

- cost of disposal.

In a typical sourcing methodology, a procurement team may realize savings in establishing strong contracts and issuing purchase orders. But too often they then hand the supplier payment process over to the finance department and accounts payable to complete the procure-to-payment (P2P) cycle.

Unfortunately, too many accounting groups think that their job is to delay supplier payments as long as possible within or beyond terms before processing invoices in the easiest manner possible. But, with a cash management strategy in place, procurement and finance can partner to deliver impressive benefits.

This article will outline five innovative methods to capture cash management advantages that enhance company liquidity and reduce overall costs.

First methodology

Do detective work. In order to strategically leverage our payment timing and processes, we first need to do investigative work. Several important areas of investigation are as follows.

1. Payment terms. Getting visibility into spending with each supplier may be easy if you’ve implemented a spend analytics technology. If so, pull data on annual spend with every supplier that also shows the payment terms established in your procurement/payables system. You’ll need to matrix the terms into several separate data elements (supplier name, supplier number, total 12-month spend, discount percentage, discount number of days and net days). But without spend analysis technology, you may need to work with information technology to extract information into good old Excel to be able to conduct your own analysis.

You will be surprised to find how many suppliers have been set up over the years with terms like upon receipt, net zero and others. As a general rule, no supplier should be paid faster than 30 days without providing a discount.

In a recent review my firm performed for a company in the agricultural sector, we found that nearly a quarter of suppliers had been set up with payment terms under 15 days. Just by moving those suppliers out to their CFO’s preferred 45-day terms, the company could free up $18 million in average monthly liquidity. (Note: Readers with a good understanding of accounting may observe that this action also moved non-accrued OPEX portions of that $18 million in payments back by 30 or more days into the next fiscal accounting period).

2. Cost of money. The next thing you need to discover is the interest rate that finance uses in its business modeling. Two alternatives here are as follows.

Cost of funds: This is typically the annual interest rate that the firm has to pay on a line of credit for funds. Opportunity cost: This is the annual profit margin management expects from a single dollar invested into company operations.

Understanding senior leadership’s approach to cost of money is essential for us to understand the perceived value of payment timing. That’s because the interest rates from these two approaches are dramatically different for the same business entity.

3. Liquidity. The final piece of information we must understand is the company’s liquidity. This will again come from the finance organization as a summary of the firm’s cash flow position. The is important because the leveraging of payment flow must be harmonized with fund availability.

I recently spoke with a CFO who mentioned that three times in the last year she had drawn upon the company’s line of credit to finance cash shortfalls. This is an example of a liquidity cost.

4. Current payment flow. For each supplier identified in step 1, you also need to find out how payments to that firm are currently made. The most common method used today is automated clearing house (ACH), which is a direct transfer into the supplier’s bank account. Your firm’s treasury bank probably charges between $0.25 and $0.50 to process each ACH direct deposit to a supplier (e-mail notification included). Buried in the monthly banking statement, you probably pay an additional batch payment charge of between $12.00 and $15.00 for each payment batch processed.

Another common method used in cross-border international transactions is payment through wire transfer. There is usually a much higher bank fee for this service of between $15.00 and $18.00, but this may be invisible to you because it’s deducted from the supplier payment. If you have smart suppliers though, they will insist the payment fee be added to their payment amount so they receive the correct net amount in their account.

Though not as frequent today, some companies still mail hardcopy checks for supplier payments. Typically performed by the accounts payable staff, this requires secure check stock paper printed on a secure printer, usually with two accounts payable staff members witnessing. Once printed, the check must be inserted into an addressed envelope and mailed with a first-class stamp.

A final form for supplier payment is the new methodology of virtual card payments, or vCards. vCard payments cost nothing to process and result in significant rebates. More will be discussed about this revolutionary payment method later in this article.

Now that our detective work is complete, we’re ready for the next step.

Second methodology

Earn rebates on “retail-like” B2B transactions. Let’s face it, the creation of a purchase order and processing an invoice makes little sense for expenditures like employee travel, fleet car fuel purchases, Internet downloads, supply purchases at stores like Home Depot or Lowes, telecommunication and utility bill payments, subscriptions, facility lease payments and a number of other expenses. The 2015 Center for Advanced Procurement Strategy (CAPS Research) Cross-Industry Benchmark Report identified the average company’s purchase order transaction processing cost to be $429. So why incur $429 to process a non-essential purchase transaction?

That same CAPS report showed that the average company spends 1.4% through corporate cards and procurement cards, or pCards. Thus, a company with $1.0 billion in total (direct and indirect) spend should be pushing at least $14.0 million through pCards. Where is your pCard program on this scale?

Having helped many companies and governmental agencies set up pCard programs, I can attest that many corporate credit card programs share some interesting “smoke and mirror” elements.

1. Cardholder incentives. Some card issuers pay no rebate to your company but offer incentives to the cardholder. These incentives make it more challenging to pry the card out of an executive’s hands. Interestingly, the full value of the incentives is almost never acted upon by the cardholder, and thus costs the issuer very little.

2. Rebate timing. Most pCard programs pay rebates annually in arrears (not monthly). That means you need to deduct half your annual cost of funds rate from the rebate to offset them holding your money until the end of the year. The math calculation here is net present value, or NPV, on the future payment stream.

3. Minimum spend requirement. Many providers pay no rebate unless “at least” $1.0 million in card spend goes through them annually, and because they pay rebates at the end of the anniversary period, you can push a year’s worth of spending through their card program before learning that you missed the minimum level and did not receive any refund.

4. Impossible rebate tiers. If a large bank does offer pCard rebates, they are often tiered at impossibly-high spend levels that the customer organization may never reach. I recently reviewed the tier levels of one retail client’s pCard provider and found that the client would have to push $1 billion in spending through pCards in order to reach the bank’s top 1.95% tier for rebates. The rebate the company was actually receiving on its $9 million annual spend was 0.75%, far below where it could have been.

5. High average transaction size. Another trick used by some bank programs is to alter the rebate percentages based on the average transaction size. This is often hidden in the fine print footnote of the program’s terms. The tiers presented in the initial proposal are for a large transaction size—often >$500 in a card-in-hand program. But the customer may not realize until a year after program implementation that the received rebates are not at the level that they originally thought they would receive. For example, an average $175/transaction size is typical for card charges of a traveling cardholder or fleet vehicle driver. And it is very difficult (if not impossible) to increase your cardholders’ average transaction size.

The good news is that best-in-class procurement card programs are now available through non-bank sources that offer dramatically better terms. For example, I recently helped a group of chemical industry companies establish a pCard program with a non-bank provider in this vertical that gave rebates starting at 1.4% at “dollar one” up to nearly 2% for high volumes of spend. The program pays rebates monthly, not yearly. That particular card issuer offered dramatically-better value to its clients than the other card programs we evaluated.

Third methodology

Utilize virtual card payments (vCard). The world of supplier payments has expanded during the last decade to include what I think is a revolutionary new secure form of payment via credit card facilities. A virtual card, or vCard, is a secure single-use payment made from a corporation’s checking account to a supplier’s credit card merchant account. The notification includes the initial card digits while the supplier/merchant has the remaining digits to process the transaction. You can pay traditional suppliers via vCard payments, just like you would with ACH, wire transfers or paper checks, pushing an AP batch payment file out to the card program provider.

vCard payments provide rebate revenue similar to a pCard transaction. But unlike traditional pCards or ghost cards, vCard payments can replace costly check, ACH or wire transfers out of accounts payable on purchase order and non-purchase order transactions. This allows inventory purchases, capital project payments, technology licensing and services and other traditional expense purchases to be settled via vCard payment.

vCard payments are a major trend today. Companies are moving away from banks for digital payment to suppliers. The “2017 Purchasing Card Benchmark Survey” results from RPMG Research Corporation One estimated that “as much as 15% of banks’ global payments revenue, or $280 billion, is likely to be displaced by the growth of digital payments and competition from non-banks, as payments become more instant, invisible and free.”

The opportunity is significant. However, it must be analyzed and implemented carefully due to games often played by traditional card issuers, including the “smoke and mirrors” tricks mentioned for pCards in the second methodology section, plus another shell game trick.

Large ticket interchange exclusions. Big card issuers often strictly impose large transaction “interchange” limitations on the rebates they pay. They sometimes do this even though the card program collected a full interchange merchant fee. These are program definitions where typical rebates are not paid because a transaction is above a certain value under the card program rules. This is frequently those above $7,500. This is the ultimate shell game trick because by moving the transaction into a large ticket interchange bracket, an issuer might exclude more than 20% of a corporate customer’s typical accounts payable payments from a full rebate.

A recent analysis my firm performed for a mid-sized client company in the manufacturing space identified between $1.7 and $2.8 million in potential vCard rebates, over-and-above supplier payment term discounts they had taken decades to establish in their $600 million annual supplier expenditures. Our review took just three weeks to conduct. Let’s face it: It’s not often that procurement can pull several million dollars in savings out of thin air in this short of a time.

A strategy in establishing a vCard program is to first choose the right card program with the right provider. Major financial firms such as American Express and Discover primarily work directly with customers, while banks or other issuers usually structure programs through Visa and MasterCard. Different levels of merchant fees charged by the program should be researched by a procurement team, as well as the level of merchant acceptance in countries where your suppliers are located because acceptance has major differences between the programs mentioned in this paragraph.

The next piece in a vCard strategy is to compare programs from different providers. This should be done by persons who truly understand the complex card space. A proper vCard analysis must ask each potential partner to match your supplier portfolio expenditures against their existing vCard payment acceptors. They can provide estimated rebate levels using your actual expenditures with companies that also accept their vCard payments. But, be very careful before solely allowing finance to ask its favorite treasury bank to estimate rebates through their pCard and vCard “programs. Get some competition involved and solicit a review from a non-bank.

A trick some legacy banks play is to match your supplier spend to a high-match list. These are lists of card-accepting merchants with accounts that are paid via credit cards or virtual cards. The problem? The supplier/merchant may never have accepted vCard payments from this issuer, instead their high-match lists tend to be comprised of merchants that merely possess an active card merchant account for receiving retail payments from their customers. This greatly overstates the real match you are likely to experience.

In reviewing card programs, you cannot merely compare rebate tier percentages, as other factors in this article make a huge difference in rebate revenues that would actually result from each provider. This truth is missed by many finance leaders when selecting a card provider. Note that the following rebate formula has two important elements: Card program spend x rebate % = rebate amount. A high rebate percentage times a low spend volume equals a low rebate amount. You get no rebate on money that didn’t go through the program.

Interestingly, the highest-volume vCard payment processer is not a bank. Nor does it issue consumer credit cards, but only corporate commercial cards. In addition to being the largest U.S. commercial MasterCard issuer, according to Accenture’s “2019 Banking Pulse Survey: Two Ways to Win,” this firm is one of the seven largest corporate card issuers. The issuer processed more vCard payments in 2019 for its customers than the four largest vCard volume U.S. banks combined.

That company converts its customers’ check suppliers to vCard payments between 26% (average implementation) and 49% (best practice implementation) of the time, compared with 17% for an average bank vCard program, according to Nilson Report, Tearsheet Research. Its success builds upon already having the largest number of vCard acceptors in the industry at nearly one million suppliers/merchants, which can largely be transformed into vCard acceptor for new customers. *

Fourth methodology

Evaluate which payment term discounts are actually being captured and take steps necessary to ensure capture. If a supplier is set up with 1% 15–Net 45 Day terms and ACH payment—that’s great. But, that also requires accounts payable to actually pay each invoice within 15 days to take the discount.

There are two problems here. The first problem is that many payables departments are instructed by their controller to extend the payment and not take the discounts procurement negotiated. Procurement often doesn’t know this. The second is that many organizations don’t process invoices fast enough to take the discounts.

This is a complicated problem to diagnose. Typically, most companies can only identify which discounts are actually being taken with a spend analysis technology solution. Otherwise, special reports need to be created to identify missed discounts. This is complicated by some companies’ accounting procedures that place captured discounts into a separate general ledger account than the actual expenditure.

Compounding this is a misconception that is held by some CFOs or controllers about payment term discounts. I can’t tell you how many of them have said something like: “A 2% discount doesn’t offset our cost of funds.” That sounds logical until I point out that a 2% 10–Net 30 discount gives them a 2% return for speeding a payment up by only 20 days. In comparison, their cost of funds percentage is an annual number. I illustrate this by telling the CFO: “If I could tell you the name of a stock guaranteed to increase 2% in value every 20 days would you buy it?”

Fifth methodology

Strategically leverage supplier payment timing to hold cash the optimal time, move suppliers toward rebate-generating vCard settlement processes, and/or move non-participating suppliers toward discounted payment terms, such as 2% 10–Net 30. This overlays the other methodologies we’ve already discussed.

In synergy with a card provider communication campaign, which should include e-mail, letters and call center phone calls (at the provider’s cost), a company can offer its suppliers several options for payment, in descending order of preference. For suppliers currently set up with lengthy payment terms, offer them shorter payment timing in exchange for accepting a rebate-producing vCard payment. For suppliers currently set up with abnormally short payment timing, such as Net 15 days, let them know that timing will no longer be honored and give them a choice of longer terms or a vCard payment. That will nudge them toward your vCard program.

Cost savings can be calculated based on the cost of money percent multiplied by the average extension in payment timing, the vCard rebates identified, and new payment discounts negotiated.

To capture new payment term discounts, many company leaders don’t know that they must be entered into the ERP system vendor master record for the supplier and that a change order must be created for every one of the supplier’s existing purchase orders. Merely updating the vendor record will not insert the new terms into any previously-existing purchase orders, including blanket purchase orders.

Achieving value

In procurement, we all want to generate savings through lower costs. However, great value can be achieved when procurement groups look beyond upstream cost savings through strategic sourcing and category management; by augmenting that with additional benefits from optimizing their payments to suppliers.

Innovative card program providers in this space are doing to payment processing what has happened to bookstores and taxi services in years past.

SC

MR

More Finance

- Investor expectations influencing supply chain decision-making

- ISM reports manufacturing sees growth in March, snaps 16-month stretch of contraction

- Supply Chains Facing New Pressures as Companies Seek Cost Savings

- February retail sales see annual and sequential gains, reports Commerce and NRF

- A New Model for Retailer-Supplier Collaboration

- How to Create Real Retailer-Brand Loyalty

- More Finance

Latest Podcast

Explore

Explore

Business Management News

- Joseph Esteves named CEO of SGS Maine Pointe

- Employees, employers hold divergent views on upskilling the workforce

- April manufacturing output slides after growing in March

- Q1 sees a solid finish with positive U.S.-bound import growth, notes S&P Global Market Intelligence

- 6 Questions With … Sandeep Bhide

- MIT CTL offering humanitarian logistics course

- More Business Management

Latest Business Management Resources

About the Author

SCMR Staff

Follow SCMR for the latest supply chain news, podcasts and resources.

Follow SCMR on social media.

@SupplyChainManagementReview on Facebook

@SCMR on Twitter

SCMR on Linkedin

Subscribe

Supply Chain Management Review delivers the best industry content.

Editors’ Picks